Decision making can be difficult–especially financial decisions-better yet-business financial decisions. Let’s lay out two scenarios and see if we can spot their underlying similarity. In situation number one, a cash-strapped consumer is contemplating choices on a lunch menu. If he purchases a mouthwatering burger, beer, and seasoned fries—a $30 lunch in this economy—he’ll only be able to fill up 75% of his car’s gas tank later.

In scenario number two, a small business owner has $5000 to improve consumer sentiment about his business. He could use that to remodel his business space or pay two dozen social media influencers to boost his brand’s online visibility.

What both scenarios have in common is decision-making. One seems like a very small-scale decision. The other appears to carry substantially more weight. But all types of decision-making have consequences.

Sometimes, those consequences are dire. Sometimes, they are so bad that they cause an entire corporation to capsize. So, if you’re an SMB owner, how do you make the right financial decision? How can you have your burger combo and fill up your gas tank?

What is Financial Decision-Making?

Financial decision-making is all about making choices to meet financial goals. Most business owners don’t have a crystal ball (except maybe fortune tellers and psychics), so it’s difficult to see how a decision will pan out.

When a financial position is personal—should I spend $5 on a latte every day or save it up for an annual vacation—its consequences tend to impact one person (the decision maker) and their immediate surroundings. However, financial decisions involving a business can affect dozens or even millions of people.

The following are a few business decisions that had Titanic consequences: Kodak, despite being at the forefront of digital photography, failed to monetize it, instead continuing to focus on traditional film. Motorola, an innovative force in cell phone technology, failed to invest in smartphone development. Circuit City tried to cut costs in 2007 by firing many of its most experienced employees, but less experienced staff could not manage.

The list goes on and on. Hindsight is 20/20, as they say. But when you’re in front of a decision, you just have to do your best. As it turns out, you can only do your best when you have the necessary facts.

The Psychology Behind Financial Decision-Making

Decisions are often made with a mix of fact-gathering, logic, intuition, and emotion. You might think personal decisions (should I ask this coworker on a date) differ from financial decisions. But reality shows a different story. Take the stock market, for example—amateur investors routinely make investing decisions from emotional spaces of panic or overconfidence.

Recessions and crashes are two situations when falling prices motivate investors to pull out of a position from a place of panic. As more and more investors sell off their shares, and available shares saturate the market, the price per share also drops—a vicious cycle that continues the trend of stock prices falling. This is an example of a financial decision made from an emotional space.

This emotionally driven investment freefall exemplifies how cognitive bias can interfere with decision-making. Cognitive bias is a broad term that includes many errors in thinking through a decision. In this case, loss aversion is the specific type of cognitive bias at work.

Loss Aversion

Loss aversion suggests that the feeling of “pain” from loss twice as acutely as the “pleasure” of gain. In a study conducted from 1981 to 1983, a 10% increase in the price of eggs led to an 8% decrease in demand, while a 10% decrease in price led to a 3% increase in demand. What the cluck?

In simple terms, as egg prices rose, demand fell. As egg prices fell, demand rose. Fair enough. But the 11% difference in consumer demand between both scenarios indicated a stronger reaction to losing money (higher prices) than saving money (lower prices)

Confirmation Bias

Another type of cognitive gap is called confirmation bias. Confirmation bias occurs when an individual only takes in information confirming their preconceived biases (e.g., opinions) while ignoring information to the contrary.

For instance, a potential franchise owner may have an emotional attachment to a specific neighborhood. When conducting market research, he will only look at data that supports the idea of opening a franchise there while ignoring all data suggesting it’s a bad idea.

Key Principles for Sound Financial Decision-Making

We’ve seen some examples of bad financial decision-making at work. It’s easy for emotion or lack of information to occlude the power of perception. So, how can an SMB go about making good financial decisions? It’s as simple as following a four-part framework.

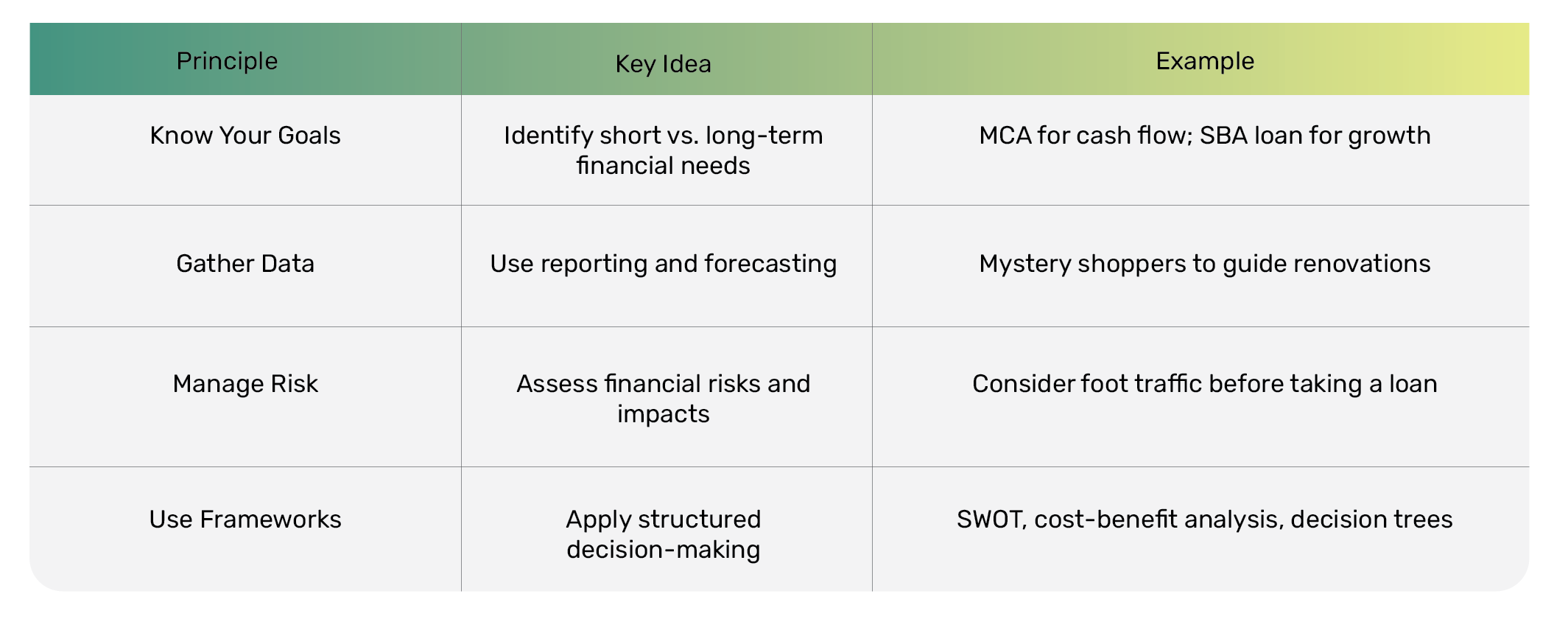

Principle 1: Know Your Financial Goals

First, know your financial goals. Are they short, or long-term? A business owner who wants to survive a short-term cash crunch and cover his or her payroll might consider something like a merchant cash advance.

An MCA can be more easily obtained than a loan from a financial institution. There are far less stringent qualifications, like the merchant’s credit score. On the other hand, a merchant interested in increasing the long-term profitability of a location by giving it a much-needed renovation may want to consider an SBA loan, provided they have a high credit score.

Principle 2: Gather Relevant Data

Reporting and forecasting are two essential processes that must be applied to collected data. Let’s roll with the example of a business giving itself a much-needed facelift. Such a business would do well to hire a consulting firm to send in mystery shoppers.

Mystery shoppers could help pinpoint which parts of the business are most unappealing. With this information in hand, the business could allocate money to whatever would have the most impact to improve consumer perception.

Principle 3: Risk Management

Business owners must identify potential risks in their decision-making. For instance, if a merchant were to consider a cash advance they must acknowledge the impact it may have on their cash flow. They must consider if nearby retail pads are emptying out. The decrease in nearby foot traffic could result in a lower sales volume for their own store–also making it more difficult to pay off any type cash advance.

Principle 4: Use a Decision-Making Framework

Utilizing a decision-making framework can limit the influence of emotion and help bring logic to the fore. Consider the following:

- SWOT analysis list a given decision’s strengths, weaknesses, opportunities, and threats.

- Cost-benefit analysis is a similar idea that compares the costs of a decision to its benefits.

- Decision trees list a roadmap of a decision and all its possible outcomes, tallying the positives against the negatives.

Tools for Better Financial Decision-Making

Mathematician David Slansky once wrote a fascinating book called The Theory of Poker. In this book, he outlined a few math-based core strategies that could be used at the card table, such as calculating “pot odds.” Pot odds compare the likelihood of winning a poker hand to the ratio of chips you will win. For instance, if your odds of winning a hand are 1:5, you should only play the hand if you win five or more chips for every chip you put in.

In simplest terms, you will lose this hand four times and win once. Each time you lose, you will lose one chip. When you win, you will win five chips, coming out of the whole experience ahead with a profit of one chip. Although this is an oversimplification, if the same logic is applied to a lifetime of poker playing, the actual results will approach these odds— just like flipping a coin 1000 times will come close to 500 heads and 500 tails.

What does this have to do with making business decisions? Namely this: the importance of financial data–everything comes down to numbers. And numbers cannot lie. The question is, how you can get a hold of these numbers to make informed decisions?

How To Analyze Financial Data

That’s where financial management software comes in. Though financial advisors may be the obvious choice when making the best decisions for your business, online accounting suites like QuickBooks can help put all the numbers in one place for further analysis. For consumers and sole proprietors (like 1099 contractors), there are now many apps like Mint and YNAB.

Once upon a time, you would have to send these numbers off to a financial services consulting firm to comb through, ponder, and extrapolate insights that might be unobservable to the naked eye.

However, cloud software has greatly democratized analytical processes. There are several very affordable tools that SMBs can access to analyze financial performance, like Tableau or Power BI, which integrate with accounting software to crunch the numbers and make predictions about the future. These predictions are devoid of emotions that might cloud human decision-making.

Steps to Improve Your Business Financial Decision-Making Process

In addition to the four principles outlined above, here is another four-step paradigm for fine-tuning the decision-making process. Speaking of poker, Let’s head over to Las Vegas and visit the oldest casino, the Golden Gate, and look at an actual problem they encountered. Although we are not privy to discussions they had around this topic, we can make some conjectures and use our imagination to illustrate these steps.

Step 1: Identify the Financial Problem or Opportunity.

In addition to being the oldest casino in Vegas, the Golden Gate was famous for its fifty-cent shrimp cocktail. However, at a certain point, the owners realized that they were losing $300,000 a year on this two-quarter treasure trove of seafood in cocktail sauce. The obvious problem here is losing several hundred thousand dollars a year (incidentally, losing money on food services is a problem that hotels frequently encounter).

Step 2: Analyze the Available Options

A few immediate options are apparent: raise the price, keep the cost, or discontinue the shrimp cocktail entirely. There are many factors to consider, such as how much of a pull the shrimp cocktail had on bringing gamblers onto the casino floor. This information might be hard to quantify without conducting a poll. For instance, guests could be given a simple survey asking them to identify the top 4 reasons for visiting the Golden Gate over other casinos.

Step 3: Consider Short-Term vs. Long-Term Impacts

Eighty-sixing the shrimp cocktail would have immediately tangible benefits, such as eliminating $300,000 in losses annually. But what would the long-term impact be?

Casinos frequently tried to outdo each other in terms of perks and incentives. Eliminating a popular feature of the casino night sends returning guests away. They might go to Binions, which featured a $2 stake as recently as 2006, or El Cortez, where you can still find a 50-cent breakfast.

Step 4: Consult with Experts When Necessary

Sometimes, it’s best to bring in an expert. Financial advisors with analytics firms specialize in observing a situation, capturing relevant data, and analyzing trends within the data to forecast predictions. If you’re wondering whatever happened to that shrimp cocktail, the owner of the Golden Gate moved it across the street to his newest property, the Circa, where you can enjoy it for $1.

However, it’s only $1 between 3 and 5 am. At all the other times, it’s $11. You can bet your bottom dollar that’s some serious-based analysis, along with considering other factors, such as consumer perception, when entering that price change.

How to Avoid Common Financial Decision-Making Mistakes

Financial forecasting techniques typically involve examining key takeaways from financial reports like accounting suites and inventory management software. These financial forecasting tools can help avoid cognitive biases in financial decisions, such as confirmation bias, loss aversion, and emotion in general.

But, sometimes, tools for financial planning can be misleading. In the process of trying to avoid financial decision mistakes and over-relying on financial decision frameworks, SMB owners can ignore their good old intuition. And sometimes intuition plays a significant role in making good personal and business financial decisions.

Although Malcolm Gladwell’s Outliers is not specifically a book about financial decision-making psychology, it does examine some fairly interesting rags-to-riches stories. In one captivating chapter, Gladwell discusses the story of immigrants to New York who started the garment and grocery store industries.

Trusting Intuition

These unlikely individuals didn’t have any software-based financial decision-making tools. They weren’t (yet) running multi-million dollar enterprises like Shoprite, Kohl’s, or Kroger. They just wanted to know how to make better financial decisions for their own personal life…like how to pay their rent and feed their family.

But they had something that even the best financial decision-making trends can’t help with intuition. Specifically, intuition honed by 10,000+ hours of practice in their profession (what Gladwell concludes is a sort of golden rule for becoming an expert at anything). With their expertise, they could pinpoint opportunities as soon as they saw them…such as the need for specific garments or food services.

There’s a decent chance you have some intuition about your industry based on years or decades of experience. When it comes to personal financial decision-making, intuition may be too closely related to emotion or bias. But don’t entirely ignore your intuitive hits when it comes to business.

Intuition can complement data-driven strategies that incorporate number-crunching and financial risk management. Walt Disney had little precedent to suggest that an immersive-themed world would become a financial success.

Today, Disney Parks generate nearly $33 billion per year. When planning and budgeting for financial decisions, do not entirely ignore the voices in your head. Unless, of course, they are actually voices in your head.

Future Trends in Financial Decision-Making

The best financial decision-making practices continue to evolve. Data-driven financial decisions are being informed by earnings reports as much as they are by new technology such as in-store tracking (e.g., seeing how customers walk around a store). Other factors, such as the increasing complexity and fragility of supply chains, are changing financial decision-making strategies.

The key to unraveling this complexity and breaking down the tidal wave of data is analytics. Today’s analytics are AI and ML (machine learning) driven, as these technologies can outpace the human ability to comb through vast troves of data.

Large companies like Amazon and Walmart are leading the way in these fields since they have the most data to analyze. Walmart even has its own data command center, the Data Cafe, in Bentonville, Arkansas. Amazon has six large data analysis centers throughout the United States, in Seattle, New York, Santa Monica, and Boston.

However, other exciting trends in analytic software have opened up these abilities to businesses and even private individuals. For instance, banking apps can tabulate personal finances and deliver consumers a rundown on their personal finances, complete with suggestions about how to save money (do you really need a subscription to Netflix, Disney+, and Hulu?).

In summary, the future of financial decision-making for businesses and consumers will increasingly be shaped by AI, ML, and cloud-based applications.

Conclusion

Assessing data powered by AI and ML can deliver incredibly nuanced insights that once would have taken an entire consulting firm to provide. For consumers, it could mean better saving, investing, and financial stability.

For business owners, this means improving the bottom line of their financial situation. The entry point for these reams of “big data” is almost always the point of sale. Payment processing captures every transaction and all its facets. POS terminals and online payment gateways record all sales metrics over a given time period (day, week, month, year), which can then be delivered to analytic software.

A robust point-of-sale solution is vital for feeding the analytic tools the data it needs and ultimately assessing your risk tolerance for new decisions. Should we stop carrying this product or providing this service? Should we pair it with other products or services? A robust payment processing solution can answer questions like these.

If you want to learn more about how payment solutions can help you make better financial decisions, contact ECS Payments today.

Frequently Asked Questions About Financial Decisions For Businesses

You can improve your financial decision-making by utilizing the following four principles:

1) Know Your Financial Goals: Set clear, measurable goals to guide your decisions. Without goals, you have no frame of reference and can easily go off track.

2) Gather Relevant Data: Use your reporting and forecasting analytics to make the most informed decisions based on your actual business conditions.

3) Prepare With Risk Management: Identify and evaluate potential risks associated with each decision. And prepare for any negative outcomes.

4) Use financial tools and resources: Tools like SWOT analysis, cost-benefit analysis, and decision trees can bring objectivity and structure to decisions. And of course, an accountant and financial advisor can readily prepare you.

There are many tools your business can utilize to help with better financial decision making. Financial management software like QuickBooks, Mint, and YNAB help businesses to organize their finances, track their spending, and create accurate business forecasts. Tools like Tableau and Power BI integrate with accounting systems for a deeper financial analysis and business forecasting, to help eliminate any emotional influences.

Mistakes to avoid in making financial decisions for your business include:

– Avoiding or delaying decisions due to fear of risk. Rather, prepare for any outcome-positive or negative.

– Making decisions solely on your emotions rather than factual data.

– Ignoring cognitive biases, which can lead to skewed decisions.

– Over-relying on financial frameworks while ignoring industry intuition.

Decision-making frameworks provide structure, reduce emotional influence, and highlight both risks and opportunities. Using the right framework ensures decisions align with the business’s long-term goals and can make the difference between sustainable growth and costly setbacks.