If you own a business, I wouldn’t be surprised if you told me you’re bombarded by messages that new technologies are either going to revolutionize your business or threaten it in some way. While some of this messaging is hyperbole and overall market hype, there is some truth to it when it comes to certain technologies. The key as a business owner is to find ways to peer into all the noise and try to see the signal that can help you navigate these fast paced changes.

Fintech and overall payment technologies have seen tremendous change and growth over the past several years. New forms of payment are emerging, and consumer behavior is changing along with them. One of the most significant changes is the move toward contactless payments for small businesses. Contactless payments were already on the horizon, but COVID-19 pandemic era regulations and behaviors fast forwarded their adoption.

Now, consumers prefer contactless payments for convenience, speed, and other reasons beyond the original accelerated adoption witnessed during the pandemic a few years ago. The adoption of contactless payments is likely a precursor and blueprint for how other new technologies will be adopted in the payment space.

To help you understand the benefits of contactless payment in real-world terms, we’ll cover several case studies showing their impact and benefits.

Mastercard’s Real World Success Stories Of Contactless Payments

Mastercard witnessed tremendous adoption with contactless payments. It has leaned into that growth recently with targeted campaigns and AI analysis to further adoption among users and merchants.

In 2019, Mastercard recorded about 30% of payments were contactless worldwide. However, by 2020, that number had risen by 40%. The fastest growth was in grocery and pharmacy, likely spurred by hygiene concerns as well as speed.

Mastercard found that nearly 80% of global consumers regularly used contactless payments when shopping in retail locations. Considering that just over a year earlier, contactless payments made up 30% of transactions, that shows incredibly fast adoption globally.

In some global markets, Mastercard has seen 90% usage of contactless payment systems for SMEs.

More interestingly, 50% of global customers stated they swapped out non contactless payment options and replaced them with contactless options. This includes choosing a new card to use or a new payment method altogether.

Mastercard has used the information it’s gleaned from contactless adoptions to create a three step initiative to further adoption and maximize the benefits for both customers and merchants. It has also created contactless payment success metrics to measure trends and adoption rates.

While these methods pertain to contactless payments, they will likely be the blueprint for new payment methods that customers show interest in.

Conversion and Activation

Mastercard found that a carefully planned rollout and implementation strategy inevitably drives adoption among consumers.

Part of that strategy involves acquiring banks and payment processors to aid merchant conversion. This means helping merchants with the technology they need to provide contactless payment training for employees. It also means providing the technical support to overcome any challenges they may face with integration.

Next, issuing banks can work with Mastercard or other payment companies to decide the best way to roll out contactless payments to their customers.

For example, an issuing bank can choose their most suitable customers first and offer them the new payment method. The issuing bank can then gather insights and metrics into the overall satisfaction and use of the new technology.

Another option is to simply do a widespread rollout. This can quickly drive adoption. However, if the technology is not well liked, it can cause problems with consumer satisfaction and even customer support.

Mastercard specifically uses AI models to predict which models will work best in the future. Merchants and issuing banks can access these models’ results to gain their own insights into the marketplace.

Promoting the Usage of New Contactless Technology

Mastercard found that segmenting consumers into distinct usage tiers could further enhance the adoption of contactless payments. The segmentation framework hinges on the key insight that consumers tend to increase both their spending amounts and transaction volumes as they use contactless payments across a wider array of merchant categories.

As cardholders advance through various engagement stages, their in store point of sale transactions are increasingly converted to contactless ones. This trend leads to a growing preference for the convenience and efficiency of contactless payments, reinforcing their favorability among users.

Mastercard refers to this strategy as lifecycle optimization. A successful lifecycle optimization strategy involves pinpointing each cardholder’s maximum engagement potential. Then, it crafts a tailored communication plan to achieve that metric.

This potential is determined by several factors including:

- the cardholder’s overall spending capacity

- the frequency of their in store transactions

- the categories in which they utilize their card.

By examining these elements, targeted strategies can be developed to maximize engagement and usage when comparing contactless vs. traditional payment methods.

Overall, the Mastercard case study shows us that contactless transaction trends in small businesses rely on cooperation since the consumer isn’t the only player. The issuers, card networks, acquirers, and merchants must all work together to find the right strategy.

This creates the best user experience for cardholders. It also increases sales and ticket amounts for merchants engaged in the adoption process.

Lauder Institute, Wharton School Study On Contactless Payments In Asia

This study examined contactless payment trends in Asia. It also examined how regulatory changes impacted adoption and what roles merchants, financial networks, and consumers all play in the adoption rate of contactless payment.

The Role of Super Apps in China

The study also looked at mobile apps like WeChat Pay and Alipay in China, two of the largest payment apps measured by active users and transactions. WeChat and AliPay are considered “super apps” for secure payments, which combine various functions with payment features.

For example, a super app will contain social media features, shopping features, and the ability to store funds, add funds from bank accounts, and make payments. These features are all seamlessly integrated. There is no need to leave the app or sign on to other services.

Super Apps in Western Markets

Super apps have been slow to arrive in Western markets, but they are extremely popular across Asia. More specifically, China, where they have become ubiquitous for retail and online payments.

Since super apps facilitate contactless payments, they are crucial to understanding adoption and what the future holds for them.

As super apps move to the United States and Europe, the results of Asian adoption will likely influence how banks, payment processors, and merchants choose to adopt and present the technology to consumers for maximum benefit.

Economic and Demographic Influences on Digital Payments

In 2017, the World Economic Forum reported that China had 224 million unbanked adults, while India had 191 million. A 2021 World Bank report predicts Asia will surpass 50% of global GDP by 2040, shifting the economic center of gravity. China and Singapore are among the world’s most digitally advanced nations, with China achieving this rapidly.

However, Asia’s diverse demographics and economies create different dynamics across the continent. Key drivers for digital payments include mobile internet expansion, data for credit scoring, and evolving regulatory frameworks.

Southeast Asia, for example, is advancing due to regional financial integration and the adoption of ISO 20022 for streamlined communication between payment systems.

ISO 2022 is an ISO standard designed to standardize communications between financial institutions. Much of this standardization revolves around messaging services between services and financial institutions.

The fact that ISO 2022 helps with adoption in Southeast Asia points to how crucial standardized protocols are among contactless payment technology providers. Once the standards are in place to facilitate secure and efficient communications, adoption comes soon after, as many products can be built up to the standards.

This standardization also allows startup fintech firms to enter the space and significantly increase the speed of innovation, as more companies are now driven by profit incentives and being first movers in the marketplace.

Challenges and Opportunities in Adoption

Bilateral agreements also help to facilitate integration, while China’s flexible regulatory start and India’s minimal requirements have both accelerated digital payment adoption.

What makes that revelation interesting is that while standardization is key to furthering the adoption and usage of new payment technologies, regulatory attitudes need to be flexible.

Difficult regulatory environments can hamper adoption and cause certain markets to miss out on advancements and the financial benefits these technologies can offer.

This is likely one reason that super apps have been adopted more slowly in the U.S. and Europe, as financial regulations are generally stricter in those areas.

In conclusion, what this study found is likely to become a blueprint for how contactless payments and other new forms of payment can grow in different markets. It also brought light to obstacles that exist and what methods, regulations, and standards can help to overcome those challenges

Country Specific Payment Infrastructures

Asian countries are building digital payment infrastructures tailored to their demographics, technologies, and regulations. This shows that there is no “one size fits all” payment technology when viewed holistically. On the surface, these payment methods may use similar technology, such as apps or tokenization. However, the underlying nuances need to be customized for the geographic area and existing framework.

In India and Indonesia, state led systems like UPI and BI-FAST have fostered competitive landscapes to help drive more innovation through free market style incentives. Conversely, China’s private led systems, dominated by WeChat and Alibaba (AliPay), have resulted in a more concentrated market.

The Future of Digital Payments in Asia and Beyond

In Singapore, incumbent banks, in partnership with the government, drive innovation. These new platforms will revolutionize point of sale payments and financing, making digital first options more viable. Those banks can also help with contactless payment compliance issues.

For the United States, the model in Singapore and the challenges it faced are likely similar to those in the U.S. marketplace.

Additionally, digital coins are set to become a preferred payment method, positioning Asia at the forefront of digital payment trends and driving economic growth. The evolution of digital payments in Asia will continue with increased innovation and competition.

The Role of Cryptocurrency and Blockchain

Cryptocurrency and blockchain technologies are both poised to revolutionize the payment industry. While direct use of cryptocurrency is unlikely to become a dominant payment option in countries like China or the U.S., the underlying blockchain technology will likely influence payment trends.

Smaller markets within countries may see cryptocurrency and blockchain adoption first, as those currencies can solve problems that may be facing the local currency in the area. Digital currencies also make cross border payment easier, which is attractive to those in smaller markets looking to extend their reach and opportunity.

Overall, this study gives great insight into Asian markets’ trends in contactless payments and payment apps and how those trends may translate to other markets around the world.

Federal Reserve Bank Of Boston Case Study

The Federal Reserve Bank of Boston examined contactless payment adoption, specifically by transit services around the United States. The goal was to determine what payment methods consumers and riders actually liked and what the benefits or challenges were when implementing those methods.

Types of Contactless Payment Platforms

The study essentially started by evaluating contactless payment platforms. One was what they classified as “closed loop” systems. This includes prepaid smart cards with near field communications (NFC) technology. The transit system supplied these cards to consumers who could reload them at various kiosks or online.

The second type was deemed “open loop” contactless payments. These included cards from outside the transit system’s control, such as Visa, Mastercard, and even digital wallets or smart devices connected to credit and debit cards.

Standards in Contactless Payments

The Federal Reserve Bank of Boston study found that standards are crucial for the success of contactless ticketing in mass transit systems and for fostering wide consumer acceptance across different transportation networks.

Standards help to establish communication protocols between cards and readers, ensuring interoperability for various applications such as transit, banking, retail, security, and building access.

Standards also allow operators to purchase products from different vendors that can function at multiple venues. In the U.S., the technical standard is ISO/IEC 14443.

Barriers to Adoption

It was found that a significant barrier to the widespread adoption of contactless ticketing in the U.S. was the need to coordinate transit authorities, municipalities, financial institutions, and technology providers to develop interoperable systems.

This is similar to what was observed in the Asian study, confirming that standardization is the key to adopting any new payment technology.

The study also cites pilot programs for open loop contactless payment in Utah, New York City, and Ohio. These pilot programs were met with great success and satisfaction with riders within the transit systems.

Pilot Programs and Cost Savings

The study also found that switching to contactless open loop methods presented considerable cost savings compared to cash collection. This is applicable to merchants in other industries and retail sectors who currently deal in high cash volumes. Switching to contactless can greatly reduce your cash handling costs and inefficiencies.

Challenges of Consumer Adoption

Finally, the study looked into the challenges of implementing contactless payments and found that “consumer inertia” or habits are one of the biggest barriers.

Consumers tend to have habits, and breaking those habits is difficult, even if doing so brings benefits and cost savings. Similar to the Mastercard study, consumer education and segmentation were key to overcoming this barrier.

Segmenting consumers into their different habits and tendencies allowed for more direct messaging to convince them of new payment options that could benefit both them and the merchant (the transit system in this case).

Security concerns with contactless payments were also a barrier, but once again, information and education can help overcome this challenge. This shows that consumer education is key to overcoming contactless payment adoption barriers across different markets and countries.

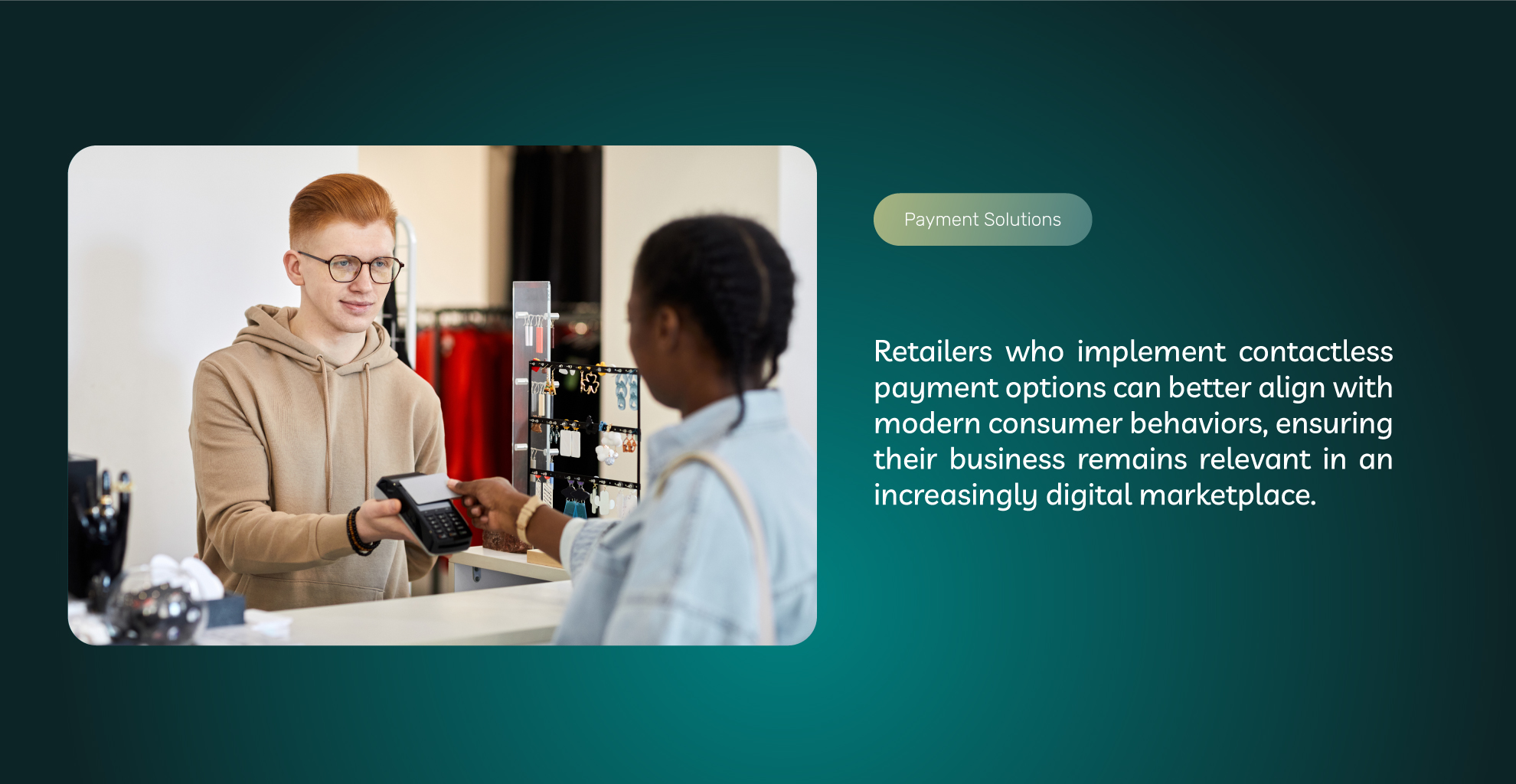

Benefits Of Contactless Payments In Retail

So far, we’ve mostly discussed adoption rates and what influences them. But contactless payments are more than just getting users adjusted to them. This technology can bring great benefits for merchants, and it’s a reason to embrace new contactless payment methods as they emerge.

Faster checkout

Transactions are quicker compared to traditional payment methods, such as dipping a card with a chip. Faster transactions reduce wait times and speeds up the checkout process, leading to increased consumer satisfaction and potentially higher transaction volumes, especially during peak times.

This is especially important for bars and restaurants. A busy bar area needs to process payments as quickly as possible. Doing so improves the customer experience and reduces labor costs since fewer employees are tied up processing payments.

Improved Customer Experience

Contactless payments provide a seamless and convenient experience for customers. They can quickly tap their card or device without entering a PIN or signing a receipt, which can enhance customer satisfaction and increase ticket sizes.

Enhancing SME Revenue Through Contactless Payments

The ease and speed of contactless payments can encourage impulse purchases and reduce the likelihood of abandoned transactions, potentially increasing overall sales. The positive impact of contactless payments on sales has been observed across several case studies, including the ones presented here. The cost of contactless payment implementation is well worth the investment.

Enhanced Security

Contactless payments use advanced security features such as tokenization and encryption, which reduce the risk of fraud and data breaches. This can help protect both the merchant and the customer from financial losses.

Reduced Cash Handling

Contactless technology in small retail businesses can reduce the amount of cash they handle, leading to lower risks of theft, errors, and the costs associated with cash management, such as counting, storing, and transporting cash.

Lower Transaction Costs

Some contactless payment methods may have lower transaction fees compared to traditional credit or debit card payments, helping merchants save on processing costs.

Contactless Payments And Customer Loyalty

Businesses can integrate contactless payment systems with reward and loyalty programs, allowing merchants to easily track customer purchases and offer personalized incentives, further improving customer experience with contactless payments.

Meeting Consumer Trends

As consumers increasingly prefer digital and mobile payment options, offering contactless payments helps merchants stay competitive and improve customer experience.

Improved Hygiene

Contactless payments reduce physical contact between customers and staff, which is particularly beneficial in maintaining hygiene and safety in many environments, such as healthcare or food services.

Contactless Payment Processing For Startups

Startups can enjoy lower initial costs when starting with contactless payments. It also helps to future proof their business and avoid costly upgrades soon after launching.

Streamlined Payment Workflow and Point of Sale POS Integration

Contactless payments simplify and streamline operations, reducing the need for manual processing and reconciliation. As a result, you free up staff for other tasks.

Future Of Contactless Payments In Commerce

Contactless payments with NFC technology, such as payment cards or digital wallets, are already being fully adopted by consumers as their preferred payment method.

However, new small business contactless payment solutions are on the horizon, and merchants need to be receptive to these new technologies so they can take advantage of the benefits.

As smart devices that use radio frequency identification (RFID) become more common, this will open up new opportunities for contactless payments. Smartwatches are already being used, but other devices or even augmented reality glasses can use contactless payments, and they have become more popular.

Biometric authentication also directly relates to contactless payments. Newer POS technology can use facial recognition or palm scanning to complete payment and further speed up the checkout process.

The more options available to find the best contactless payment methods for shops to use offer maximum flexibility and revenue generating potential for merchants.

Learn More About Contactless payment Options For Your Business

ECS Payments offers the latest digital payment solutions for businesses that want to leverage the latest technology to boost sales and reduce costs.

Contact ECS Payments today to learn more about the solutions you need to accept contactless payments and other digital solutions that can help your business seamlessly transition into the future of payment technology.What are the benefits of contactless payments for small businesses?

Frequently Asked Questions About Contactless Payments

COVID-19 significantly accelerated the adoption of contactless payments. They hype around the pandemic Increased awareness of hygiene concerns that drove consumers to prefer contactless payments over cash or traditional credit card transactions.

Contactless payments may become a challenge only when there are compatibility issues between different contactless payment systems and a lack of universal acceptance at all merchant locations. Meaning, if you are a business and have not yet implemented contactless payment systems… it’s time.

Contactless payments are convenient, fast, secure, cost effective, and can improve the overall customer experience.

To encourage contactless payment at checkout, merchants must first partner with payment providers to offer contactless payment solutions that are compatible with various devices and platforms. Then, a merchant can:

•Display signage promoting contactless payments at checkout counters.

•Offer discounts or loyalty rewards for customers who use contactless payments.

•Train staff to educate customers about the benefits and security of contactless payments.