As a merchant who accepts digital payments, you will soon realize, if you haven’t already, the many merchant service providers you can choose from and the different pricing they offer. This article will take us on an in-depth journey through merchant service fees explained in an easy-to-digest read.

Merchant Fees

Credit card fees for merchants are complicated. They are difficult to predict in many cases. This is because all transactions come with different costs.

Fees associated with payment processing explain why there is so much confusion in determining the best processor for merchants. There’s a lot out there and it’s hard to know what is the best option.

Each payment processor and card brand, such as Visa and Mastercard, has its own fees attached to facilitating each transaction. Additionally, the price can vary depending on your pricing structure, the type of card used, and the way the data was processed.

Every time your business accepts digital payment, whether a card is swiped, dipped, tapped, or keyed in, you will have to pay a fee to process the transaction.

This fee typically includes the interchange fee, plus a per transaction fee, plus additional fees such as merchant account fees that vary per transaction and provider. Below we will continue to unravel what each of these merchant fees looks like.

Effective Rate

Before sharing with you all the possible fees that you may be charged for your merchant processing, we need to answer the big question. What is an effective rate? An effective rate is the overall percentage of the cost you incur to process digital payments.

If you can determine your effective rate from each merchant service provider, you will have a better idea of which quote from which provider best suits your business needs.

You can determine your effective rate by dividing the total fees you would pay for your processing by your total credit card sales. You can do this by yearly or monthly numbers. However, month-to-month variances can differ drastically depending on the consistency of your sales volumes.

As an example, if your gross card sales are $100,000 for the year and you paid $3,000 in payment processing fees, your effective rate is $3,000/$100,000 = 3%.

Now that you know the bottom line: how to determine your business’s effective rate, let’s take a look at all the possible fees that may apply to your total merchant processing fees.

Interchange Fees

Each credit card company has a set standardized fee for each card every time it is used, along with how it is used. Interchange fees are the base fee for any merchant processing rate. The card issuing bank would charge this fee to the processor, who then passes it along to the merchant.

This fee is a percentage of the total transaction. Additionally, the fee on a certain card type will be higher if the card is keyed or swiped, when it has EMV or NFC capabilities.

These interchange fees are transparent and pre-determined. The following factors determine a transaction’s interchange rate:

- The card issuer (Visa, Mastercard, American Express, or Discover)

- The card type (credit or debit card)

- The card level (standard, rewards, privilege, gold, platinum, business, etc)

- The industry of the transaction (retail, restaurant, healthcare, etc)

- The transaction location (card-present or card-not-present)

The rates can change from time to time. However, merchants can view them at any time. You can check out the current interchange rates on Visa, Mastercard, American Express, and Discover’s websites. We have also included current rates below for your reference.

Types of Pricing Structures

When payment processors pass along the interchange rate to their merchants, they can do it in one of three pricing structures:

- Flat rate

- Interchange Plus

- Tiered

There is no one-size-fits-all when it comes to choosing the best pricing structure for your business. Some pricing structures may offer benefits that are more attractive to some business owners, while the same structure may not be as beneficial to others. It all depends on a merchant’s priorities.

With certain benefits come certain sacrifices. For example, certain structures may offer easy-to-determine set monthly fees, however, it may end up costing a merchant more money. While other structures may offer lower fees overall, however, it may not be as easy to predict what a merchant’s fee will be.

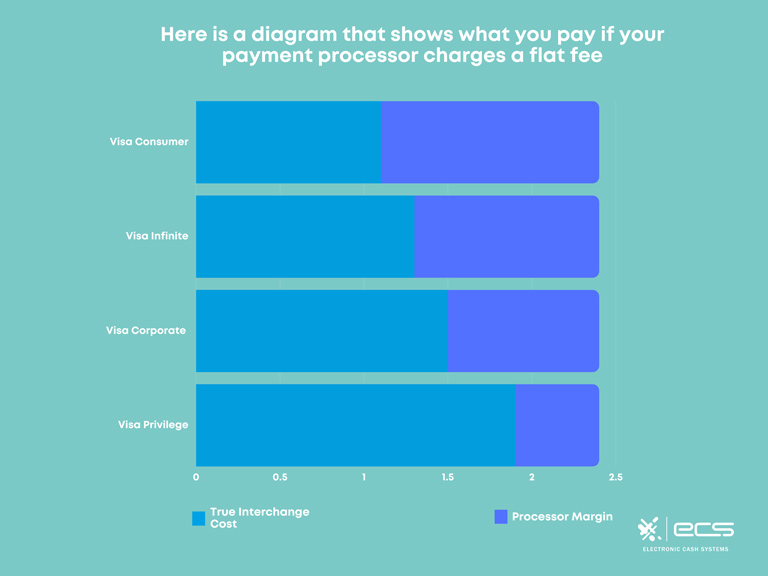

Flat-Rate Pricing Model

Flat-rate pricing is simple. It is the easiest payment structure to understand. Regardless of a transaction’s interchange rate, the rate the merchant pays remains the same.

This would be their singular flat -rate plus their set per-transaction fee. Because the interchange rate fluctuates, but the merchant’s rate remains the same, the processor’s margin in return, would fluctuate. Depending on the interchange fee, a processor may make more or less profit from each transaction.

For example, a merchant can be priced with a flat rate of 2% + a 20¢ transaction fee. No matter what card was used, the merchant will always be charged 2%. So the merchant will always know what to expect when it comes to their credit card fees.

Flat-Rate Benefits and Disadvantages

The flat rate can have its advantages and disadvantages. If we take the above example of a 3% flat rate and a certain transaction’s interchange rate is lower than 3%, the merchant will lose out on those savings. Conversely, suppose the interchange rate is higher than 3% for a certain card transaction. In that case, the merchant will reap the benefit of a lower fixed rate.

It is typically advised that merchants who have an average credit card processing of more than $5,000 per month or who offer online payments, should look into alternate pricing structures. Flat-rate pricing is generally best for in-person merchants with lower sales ticket volumes.

Let’s look at an example. If we take the merchant we mentioned above who has an average annual credit card sales of $100,000 with the flat rate pricing structure representation of 3% plus 20¢ per transaction, with an average ticket of $20, the effective rate would be: 4%

Calculations

$100,000 x .030 = $3,000 owed from annual credit card revenue

$100,000/$20 = 5,000 average transactions

5,000 x .20 = $1000 owed in fees per credit card swipe

$3,000+$1000 = $4000 total merchant fees = 4% effective rate

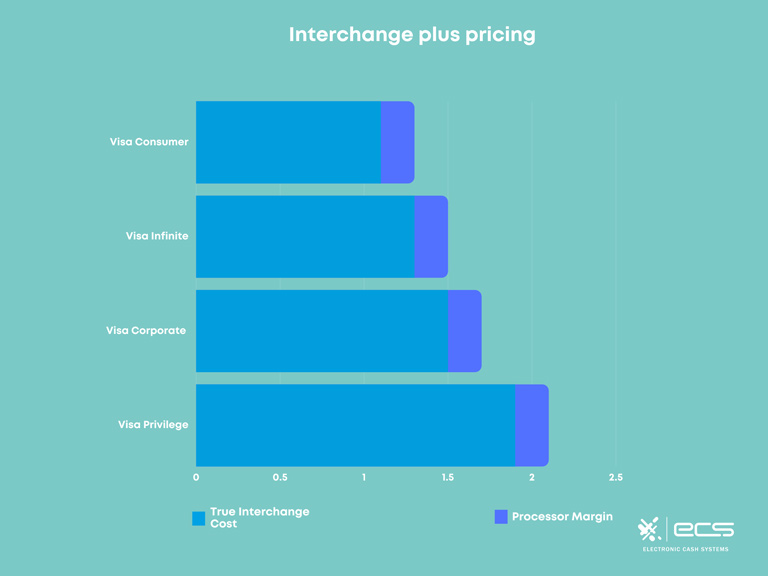

Interchange Plus Pricing Model

The interchange plus pricing model is exactly what it says it is. An exact pass-through to the merchant of the interchange rate from the card brand plus a per transaction fee from the processor.

Because interchange rates fluctuate so dramatically per card or type of transaction, the rate a merchant pays will fluctuate. The payment processor’s margin will always remain the same. Which is the per transaction fee they charge in addition to the interchange rate.

Interchange Benefits and Disadvantages

The interchange plus pricing model is the most transparent pricing structure. The rates are available to the public and listed on all the card brand websites.

Merchants can take advantage of lower rates and will never be overcharged for interchange. However, with the transparency of full passthrough, the downside is that interchange plus makes merchant fees hard to predict and different for each transaction.

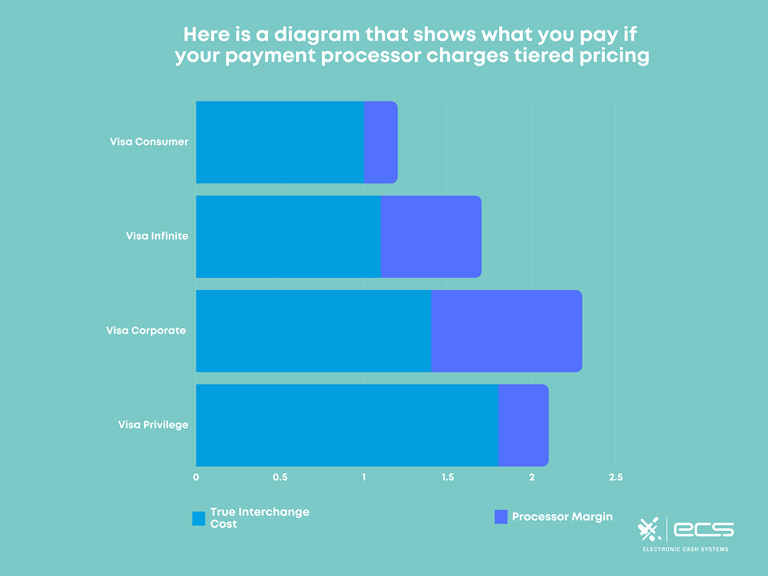

Tiered Pricing Model

Tiered pricing is the most common merchant pricing model. This structure allows for the fluctuation of fees and profits for both the merchant and their credit card payment processor.

Tiered pricing uses the interchange fee plus factors of a transaction based on risk to determine which one of four tiers the transaction will fall into for the credit card processing fees. The four pricing tiers are:

- Qualified

- Rewards

- Mid-Qualified

- Non-Qualified

The qualification category would be dependent on factors like:

- The location of the sale

- Card-present vs card-not-present

- The credit card level (rewards, business, etc)

- Credit card vs. debit card

- The captured cardholder information (name, address, etc)

- The amount of time between the card authorization and the settlement

Qualified Rate

The qualified rate has the lowest cost to the merchant. Qualified transactions are the safest. In-person payments with a low-level credit card and batched out on time receive the qualified rate.

Rewards Rate

Previously considered a part of the mid-qualified category, reward cards now have a separate rate. Any rewards cards that offer discounts for airlines, hotels, travel, department stores, etc will fall into the rewards rate.

Mid-Qualified Rate

This rate is more expensive than the qualified and rewards rate and less expensive than the non-qualified rate. Mid-qualified transactions may have been “qualified”, but the merchant keyed in the card rather than using its chip or contactless options in person.

Or if the merchant forgets to batch out within 24 hours of the sale. In this case, the risk of chargeback increases, which will then increase the merchant’s processing fee for that transaction.

Non-Qualified Rate

Non-qualified transactions are those that carry the highest amount of risk and therefore are the most costly to the merchant.

These transactions would include keyed transactions into a payment gateway without using the address verification system. Corporate or international cards. Or any transactions batched out 48 hours past the time of the sale.

Tiered Pricing Benefits and Disadvantages

Non-qualified transactions are those that carry the highest amount of risk and therefore are the most costly to the merchant.

These transactions would include keyed transactions into a payment gateway without using the address verification system. Corporate or international cards. Or any transactions batched out 48 hours past the time of the sale.

Universal Merchant Account Fees

Once you’ve established your payment processor and the coinciding pricing structure, there are still additional fees you must pay regardless of our pricing structure.

Authorization Fee

This fee applies to every card swipe, dip, tap, or key. Regardless of the transaction status, accepted or declined, the merchant will still have to pay a fee to the financial institutions to facilitate the transaction process and verify if the card is valid.

Card Brand and Network Association Fees

Card brand associations charge assessment fees to cover annual participation, fraud prevention, and other network operation costs.

Situational Merchant Account Fees

Some of these fees may apply to you and some may not. But it is best to be aware of all the opportunities payment processors may use to charge your account. These additional incidentals may appear in the fine print of your merchant contract.

PIN Debit Fee

Merchants may need to pay a monthly access fee to the debit network, around $5 – $10. Additionally, the debit network charges a 20¢ per transaction fee for each debit transaction that requires the entry of PIN verification.

Address Verification System Fee

When transactions are keyed into a payment gateway the AVS helps keep customer data secure. A 1¢ transaction fee may apply.

Return Transaction Fee

When a customer returns an item, there is a return fee as well as a transaction fee.

Retrieval Request Fee

If there is a charge a customer does not recognize, they can inform their bank. Their bank can then look into the charge to help inform their cardholder what the transaction was for. This process requires the bank to request evidence from a merchant and thus a retrieval fee must be collected.

Chargeback Fee

If a cardholder disputes a transaction with their bank, a merchant will be charged a fee to initiate and process the cardholder’s request. A merchant does, however, have an opportunity to rebuttal the dispute and prove the authenticity of the transaction.

Whether the merchant wins or loses a chargeback case, they will still owe a $15 – $25 fee for the facilitation of the process.

Batch Fee

Some processors may charge a 5¢ – 25¢ fee for settling a batch to the merchant’s acquiring bank.

Cancellation or Termination Fee

Some merchant service providers charge an early termination fee to merchants who end their contracts early.

Voice Authorization Fee

A 65¢ – 95¢ fee may be charged if a merchant has to authorize a sale via phone. This can happen if a terminal is un-operational due to a power outage, malfunction, or internet connectivity issues.

PCI Non-Compliance Fee

If a merchant fails to pass their PCI survey or become PCI compliant, they must pay a varying compliance fee depending on their payment processor. This is a penalty for not abiding by the card networks to go the full length to protect cardholder data.

Terminal Lease Fees

If a merchant chooses to lease their terminals rather than purchasing upright, they will see a monthly terminal fee on their account.

Application Subscriptions

Merchants who use POS devices like Clover have the opportunity to use additional applications to streamline their workflow. If they choose applications with subscription plans, there will be an additional charge for these on their monthly statement.

Monthly Fee

Whether a merchant processes or not, some processors charge a monthly $10-$15 statement fee to cover the costs of maintaining a merchant’s account as well as printing and mailing monthly statements.

Monthly Minimum

Some merchants have contracts that state they must process a minimum amount of credit card transactions. If they do not meet their minimum, they will have a fee applied to their account to cover the processor’s monthly fee.

Wireless Fees

To facilitate wireless connectivity for terminals, some merchants may incur a $40 – $60 setup fee, a $10 – $25 monthly wireless fee, and even a 5¢ – 15¢ per transaction fee for every transaction on a wireless terminal.

Which Merchant Fee Structure is Best?

There is no way to say one is better than the other in general. However, there are better options for different merchants based on their business type, needs, and transaction amounts.

For example, if you are a newer merchant or a small business with a low volume of sales, a flat-rate option may be the best for you to start. However, after you get up and running and start making more than $5,000 to $8,000 a month, you may want to reconsider your pricing model.

But be careful not to get stuck in a pricing model with a payment processor that does not offer you room to grow. If you decide your fees don’t suit you anymore and want to look into a new provider, breaking your contract can be costly with early termination fees.

Conversely, if you are ok with not being able to forecast your credit card fees and want to know you are saving money, the interchange model may be the best suitable option for your business.

Merchant Fees Conclusion

When it comes to credit card merchant fees, explaining the difference can help guide a merchant to their best option. The comparison between the pricing structures and the additional fees can be challenging to understand.

However, my hope is that this article has shed some light on how to determine which model is best for you and your specific needs as a merchant. Determining your credit card sales volume and knowing your priorities (predictability vs. cost), enables a wiser decision for selecting your merchant fee model.

To contact sales, click HERE. And to learn more about ECS Payment Processing visit Merchant.