Many of us in the United States likely remember receiving new credit or debit cards in the mail from our banks. These new cards had a small metal chip embedded in the front and worked with new chip readers installed at many retail locations and ATMs. These EMV chip cards provide additional security to combat fraud and unauthorized use of stolen credit card information.

However, you likely also noticed that new cards still use the traditional magnetic strip. These magnetic strips still contain card information and, in some cases, can still be used to complete transactions.

However, changes to magnetic stripe cards and EMV cards in the coming years will affect those who accept cards in person and process payments.

In the rest of this article, we’ll explain the differences between magnetic swipe cards and EMV chip cards. We’ll also explain how certain technologies will be phased in or out and whether magnetic stripes still serve a purpose moving forward.

What is an EMV Chip Card?

EMV stands for Europay, Mastercard, and Visa. This industry group came together to create the standards for the new chip cards. The goal was to create a card that was much more difficult to clone by criminals.

Over the years, criminals have become more sophisticated in creating fraudulent credit cards. Often, they would acquire credit card information via hacking or other means and then use that information to create fake credit cards with the correct account information. Fraudsters can then use these cards for purchases.

The EMV chip cards use an integrated circuit built into the card, which is much harder to clone successfully and create a fake card. The EMV chip also makes the transfer of credit card data safer, a technology we’ll touch on later in the article.

Europe was the first to introduce EMV cards. The U.S. did not introduce them until 2011. In 2015, new rules were put in place by the credit card companies that essentially shifted the liability to merchants if they did not use the EMV technology cards offered for a transaction. These penalties forced merchants to rapidly adopt EMV cards and new card readers nationwide.

What Hardware Do EMV Cards Need?

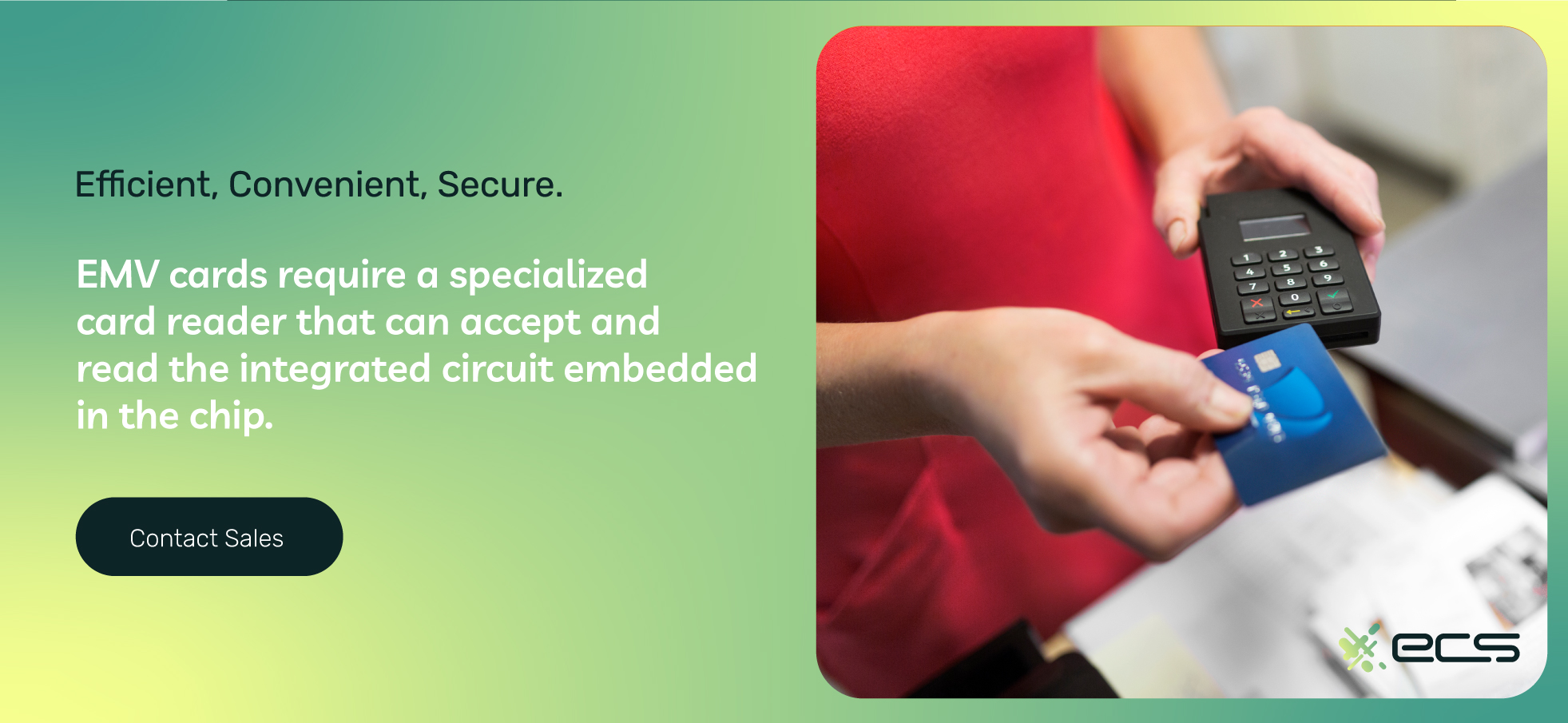

EMV cards require a specialized card reader that can accept and read the integrated circuit embedded in the chip. These readers have the customer “dip” their card into a slot in the reader. The card is then held in the reader for the remainder of the transaction until authorized.

These newer EMV card readers also have NFC or near-field communication abilities built in. Allowing the machine to read the card without dipping the chip into the machine. Instead, the NFC reader sends out a small electrical signal that activates the integrated circuit on the card. The card then transmits the information to the reader in a secure way without there needing to be any physical contact between the card and the reader.

NFC technology is also how digital wallets such as Apple Pay work to achieve contactless payments using a smartphone. In these cases, the digital wallet app communicates with the reader instead of the card itself.

Why Is An EMV Card More Secure?

EMV cards are more secure because they employ a security feature that legacy magnetic cards cannot. This benefit is one of the most critical that EMV chip cards offer.

When dipping an EMV card into a reader, the integrated circuit produces a one-time, unique code to verify the transaction. Each time the card is dipped, a new code is generated. For every transaction, the unique code must be verified.

In the field of information security, this process is tokenization. Tokenization is the transformation of sensitive information into a code or “token.” That token is sent between systems to be processed instead of the genuine raw details. Once the token is authorized, it can be discarded and is never again valid.

Another reason EMV chip technology is more secure is that reproducing the integrated circuit embedded in the cards is extremely difficult. Chip reproduction cannot be done easily or cheaply on a large enough scale for criminals to accomplish through common credit card fraud. Making chip cards much more difficult to counterfeit, removing one security issue with stolen credit card information.

EMV chip card disadvantages are relatively few; the most prominent disadvantage is they do require newer readers. That means businesses have to invest in new technology to process these cards. But overall, businesses will enjoy cost savings with lower card fraud and other benefits. They can also now accept new forms of payment that are becoming increasingly popular with consumers, such as Apple Pay or other digital wallets.

EMV Cards For Online Payments

Many businesses are solely based online and process their credit card transactions via their store and payment gateway. For these applications, the processing flow is unchanged due to the introduction of EMV cards.

For online payments, cards are run as CNP transactions or card-not-present. This type of transaction generally does entail slightly more risk. It, therefore, has a higher transaction fee for merchants who process this way. Phone orders are processed the same way.

But the payment gateways and issuing banks use different methods for fraud detection for CNP transactions. These include using filters to flag fraudulent transactions, such as the card’s country of origin, past use of the card, and the transaction amount compared to either the customer’s history or the merchant’s average transaction size.

Overall, merchants who only process credit or debit cards online via an e-commerce business don’t need to make any changes regarding EMV cards. Their payment gateways and other processing technologies will all work the same. The same billing information required by legacy credit cards is still all that is needed now when customers shop online.

How Do Magnetic Stripe Cards Work?

Legacy credit cards with a magnetic stripe work much differently than EMV Cards.

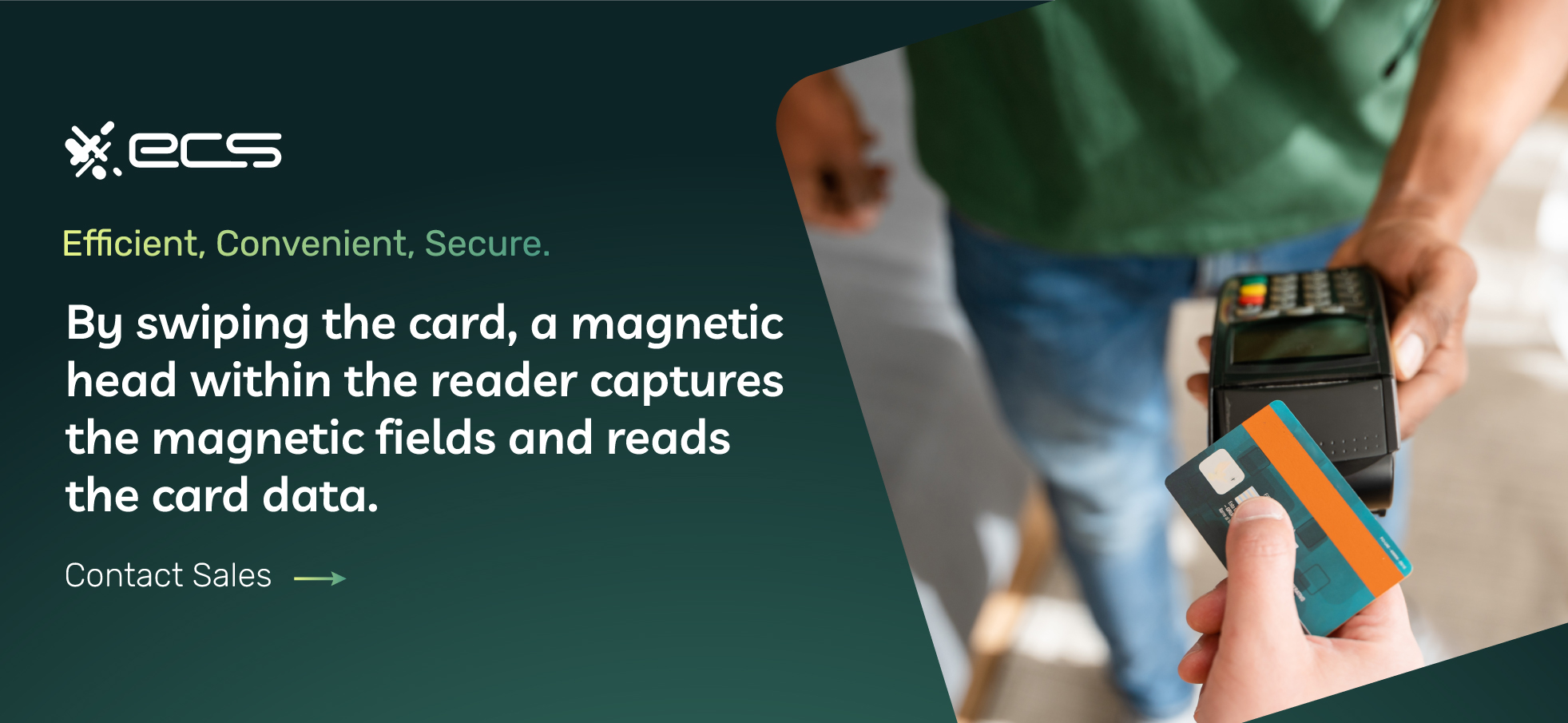

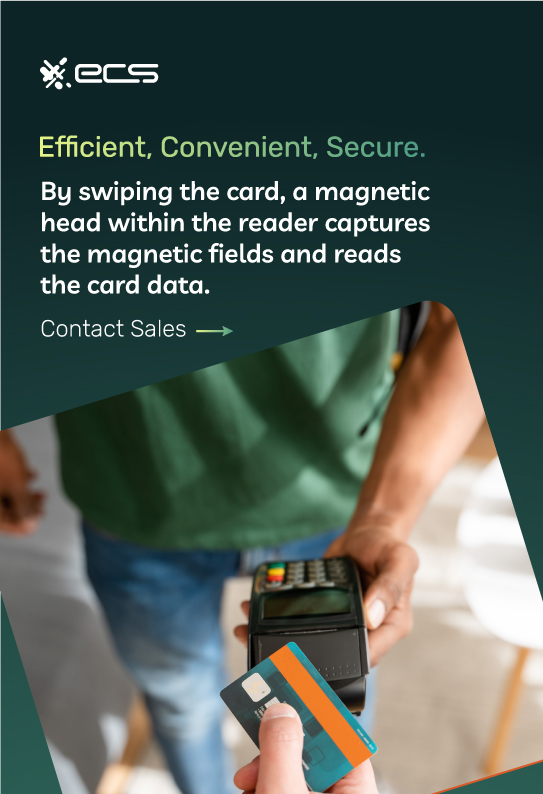

The magnetic stripe on the back holds the credit information with legacy cards. By swiping the card, a magnetic head within the reader captures the magnetic fields and reads the card data. It is then sent for payment processing.

As you can tell, compared to the EMV workflow, the data is not tokenized in this scenario. Instead, the raw card data is sent between the merchant and the processing network, which makes it far less secure. This security issue is one of the major magnetic stripe cards disadvantages and why card networks began replacing them with EMV chip cards.

Also, reading magnetic card data is straightforward. So, creating counterfeit cards once a criminal has a credit card number is not very difficult. Even an unskilled criminal can usually accomplish this task easily.

Can I Still Process Credit Cards Using A Magnetic Stripe?

Most EMV cards still have a magnetic stripe on the back containing the credit card information necessary to complete a transaction.

The magnetic stripe also contains a code that tells the reader it is an EMV chip card. If a customer tries to swipe a chip card, the reader notices the code, prompting the customer to dip the card instead of using the magnetic stripe to complete the transaction.

If the chip fails to be read or fails in some other way, the card reader or POS terminal reader may prompt the customer to swipe the card as a fallback method of completing the transaction.

This option can work in some cases, but increasingly more of these fallback-swiped transactions are being denied or not allowed. However, there is no harm in trying to run a card using this fallback method if there is an issue with the chip reader.

If the chip reader is not working, another fallback option is to key in the transaction manually. For this, the retail location will need to have a POS system installed and a virtual terminal app running on that POS system.

A POS system is an advanced hardware and software setup that retailers and merchants use to process transactions. It can offer additional functionality, such as running a virtual terminal. A virtual terminal is a software-based “terminal” that allows employees to manually enter credit card information to be processed. Merchants often use these terminals for taking orders over the phone or by fax.

However, they can also be used in a POS situation when a card reader is not working. Just remember that these types of transactions usually incur higher transaction fees since there is no way to verify the card is present.

Risks Of Using Swipe Or Keyed Transactions When Chip Readers Fail

Merchants should be careful when using fallback methods if the EMV reader fails to read a customer’s card. The fallback is relatively uncommon, so this won’t be coming up often. If it does, it may mean your card reader needs to be repaired or replaced.

But when a merchant chooses a fallback method like keying in a transaction or swiping, they are generally liable for any fraud that occurs with that transaction. This means merchants should take extra precautions if they run these types of transactions.

If you’re a local restaurant and a regular customer has trouble with their chip card, there’s generally no harm in keying in that transaction manually. However, suppose someone the merchant doesn’t know tries to make a large purchase at a retail location, and the chip does not work. In that case, running that transaction through another method with no fraud protection may not be worth the risk.

To help with this, ensure you educate your staff on how fallback methods for credit card processing work and which scenarios you feel are warranted. This way, there should be no confusion or additional risk at checkout when a terminal does not read a customer’s EMV chip correctly.

Upgrading Your Card Readers To EMV

If your business needs to upgrade its terminals to accept the latest card technologies, there are a few things to keep in mind. You likely already have EMV readers installed at your business, but there are newer card readers who take advantage of the full benefits that EMV technology now offers.

Many of the original EMV readers that merchants switched to did not have NFC capabilities. This means that customers can’t use contactless payment solutions or certain mobile payments.

If you have one of these older EMV readers, it’s important to consider upgrading to a newer system with NFC. Upgrading can speed up the checkout process and helps to give customers more options. It also puts less wear on your card reader, meaning it will last longer and must be replaced less often.

Upgrading your EMV reader also future-proofs your processing. Newer digital wallet technologies like those pioneered by Apple Pay are becoming more popular with consumers. Many consumers only travel with their Apple-Pay-enabled phones and don’t even bring credit cards anymore.

Serving these customers can increase your sales and help you stay current with the latest payment or smart card technologies.

What’s important to know is that upgrading your reader does not usually require any of your existing payment gateways or anything else to be changed.

Finally, if you want to upgrade, consider looking into POS systems if your business is still just using a payment terminal or card reader. POS systems and the latest EMV readers can offer enhanced business functionality like inventory tracking and employee management.

If your business needs to upgrade its payment processing solutions, contact ECS Payments. We offer the latest EMV readers and POS systems. We can help your business leverage these technologies to increase efficiency and profitability.

Are Magnetic Stripes Still Useful

With all the benefits of EMV chip cards, magnetic stripes and their readers have no place.

But this isn’t entirely true. While credit and debit cards are phasing out magnetic stripes, many readers still have them, and this is because there are still magnetic stripe card benefits in some cases.

Businesses may want to swipe other types of cards outside of payments. Some examples are loyalty or reward program cards. Many businesses have their rewards program integrated with their POS system. This means customers can swipe magnetic loyalty cards to receive benefits or perform other necessary actions.

Some businesses also supply gift cards not part of the credit card payment network. A magnetic stripe reader can also read these.

So even though the card brands are doing away with the magnetic strip, there are still some applications for it that businesses may still require. Because of this, newer card readers still have a swipe option. They will likely include it for some time to deal with the legacy technology.

When Will Magnetic Stripe Cards Be Completely Phased Out?

You’ve likely noticed that your credit or debit card still has a magnetic stripe. Cards still have these, but they are phasing out over the next several years.

In 2024, Mastercard will no longer require adding magnetic stripes to any card. Although card issuers can still include them if they want to, they are simply unnecessary after 2024.

By 2033, no Mastercards will have any magnetic strip, although the transition may happen sooner by choice. 2033 is when it is set to be official in the payment industry.

This means that although it’s being phased out, it is a long process until it becomes official. But for now, most merchants are already processing EMV chip cards exclusively and only using the swipe method as a fallback in unique situations where it is safe to do so or allowed.

The Latest EMV Readers To Prepare Your Business For The Future

Payment technology, consumer trends, and buying behavior are changing fast. This evolution means merchants must stay current to attract and maintain those valuable customer relationships they’ve built over time.

ECS Payments helps you achieve this by being a trusted partner to help with digital payments. We specialize in the latest payment processing solutions, including online and leading-edge card readers and POS systems.

Contact ECS Payments to learn more about the latest EMV readers and how we can help your business succeed by accepting the latest forms of digital payments.

Frequently Asked Questions About EMV Vs. Chip Cards

Most up-to-date card terminals accept EMV payments. If it’s been a while since you’v updated your equipment, it’s time. Because magnetic stripes are soon to be extinguished. Many, but not all, EMV card reading terminals also have NFC capabilities for contactless payments. Upgrading your card readers can enhance the checkout process and provide customers with more payment options. If you need to upgrade your payment processing solutions, contact ECS Payments for our latest EMV and contactless readers.

Currently, credit cards still contain magnetic stripes, but the card brands will soon eliminate mag stripes altogether. Magnetic stripes are less secure and pose a risk to you and your customers. We strongly recommend considering upgrading your payment terminals to read EMV and NFC payment cars. Contact ECS Payments for more information.

Magnetic stripe cards will be gradually phased out in 2024 and then full discontinuation by 2033. To stay updated on the latest payment technology and prepare your business for the future, follow ECS Payments on our social media platforms and subscribe to our blogs and newsletter.

Upgrading your payment terminals to the latest EMV readers helps you stay current with evolving payment technology and consumer trends. EMV terminals improve efficiency, increase security, and boost profitability. Contact ECS Payments to help guide you through the upgrade process.