Let me paint you a mental picture of why payment processing is so important to your bottom line. It’s your grand opening, your shelves are stocked, registers are staffed, and customers are lined up outside ready to peruse your aisles. Excited to purchase your goods at the newest market in town.

All you have to do is open the doors, let the public in, scan their goods, swipe their credit card, and boom! Your bank account is paid! 3 seconds and the transaction is complete!

Well…that’s not quite the case. A credit card transaction is a lot more in-depth, with plenty of other gears turning in those 3 seconds behind the scenes that you may not be aware of.

With payment processing, in a matter of seconds, your customer’s credit card information is being authorized and authenticated by the passing back and forth of information between your store terminal or online gateway, the processor, the card brand networks like Visa, Mastercard, Discover, American Express, and the cardholder’s issuing bank. Whoa, that’s a lot of information, let’s dive a little deeper and take a closer look at how this all works.

The Key Players in Payment Processing

As we have experienced above, in credit card and payment processing, there are many key players involved in the process. Each entity hands off information to the next, in an assembly line of data transfer, to process the transaction as either successful or declined.

To better understand how credit card processing works, you will first need to understand each role and who all these players are!

Merchant

A merchant is any business that sells goods or services to consumers. A merchant can accept credit card transactions via a physical or virtual terminal, where a card can be swiped, dipped, tapped, keyed, or used for contactless or mobile payment. If you are a business owner, we are talking about you here!

Cardholder

A cardholder is an individual who was issued a credit or debit card by their bank to use for purchasing goods or services; this is your customer!

Issuing Bank

An issuing bank is a financial institution and member of the card brand associations that issue credit or debit cards to consumers. It is responsible for the cardholder’s ability to complete the transaction with their line of credit or availability of funds. Upon the card authorization, the issuing bank will either approve or decline the transaction. This is your customer’s bank.

Payment Gateway

The payment gateway is the system that channels the card information from the terminal, physical or virtual, to the credit card processor, who then sends the information to the credit card network or brand (Visa, American Express, Mastercard, or Discover). Payment Gateways can be either software programmed into your POS device or an online integration into your website.

Acquiring Bank

An acquiring bank is a financial institution that is a registered member of the card brand associations. As a merchant, you will need an acquiring bank that accepts credit or debit card transactions. This bank will be submitting the transactions to the card brands, then back to your credit card processing company, and then finally into your bank account!

Payment Processor

A payment processor is a vendor that transports card information to and from your terminal, the issuing bank, the card brands, your acquiring bank, and your bank account.

Payment processors can also be an all-inclusive merchant services company. A “one-stop-shop” so to speak when getting your business started and ready to accept card payments. They would be able to provide POS systems to their merchants, as well as provide card processing services; the facilitation of the movement of funds between all the players as mentioned above.

You will most certainly want to find yourself an exceptional payment processing company, as they will be your main point of contact should you have any questions regarding the funds your account sees after your daily sales!

How Does Credit Card Processing Work?

Although it may seem like a quick and easy 3-second procedure, there are three main stages for a credit card transaction to be processed:

Credit Card Authorization: Authorization is the operation of verifying a transaction and receiving approval from the cardholder’s bank.

Clearing: Clearing occurs after a transaction has been approved. The transaction data is then sent from the processor to the card brands and issuing bank to post to the cardholder’s bank account.

Settlement: Settlement is the process of moving funds. Funds are transferred from the issuing bank to the processor/acquiring bank, and finally to the merchant.

Credit Card Authorization Process

A cardholder initiates a purchase by providing the merchant with their card information through swiping, dipping, scanning, or keying in their card information into a physical or virtual terminal.

- The merchant’s point of sale device sends the authorization request with the credit card data to the processor/acquirer.

- The processor/acquirer routes the authorization request to the card brands/networks (Visa, Mastercard, American Express, Discover).

- The card brands forward the authorization request to the issuing bank.

- The issuing bank validates the authorization by checking the cardholder’s account for available funds, verifies the card number, billing address, and CVV number, and sends an approved or declined response along with an authorization code to the card brands.

- The card brands will route the response to the processor/acquirer.

- The processor/acquirer sends the approval or decline response back to the merchant’s POS device.

- The merchant completes the transaction with the cardholder.

This all happens within 3 seconds!

Credit Clearing & Settlement

The clearing and settlement stages occur simultaneously.

This is the part where the customer’s bank account reflects the debit, and the merchant’s bank account reflects the credit of a purchase.

This step occurs hours after the actual transaction.

Most low-risk merchants are funded within 24 to 48 hours of the transaction. A successful card transaction will be posted to the cardholder’s monthly statement from the issuing bank, as well as the merchant’s transaction statement from the processor.

Payment Processing Clearing Protocol

- As the business day is concluded, the merchant must batch out their POS device and send the accepted payments and transaction data to the processor.

- The processor transmits the transaction data to the card brand networks.

- The card brands send the sales data to the issuing bank.

- The issuing bank will then send the funds to the credit card network.

- An interchange fee is removed from the total funding and is paid to the issuing bank and credit card network.

- The credit card network will then send the acquiring bank and processor the remaining funds, and these entities will be credited with their due percentage from the transaction.

Settlement Process

- The processor submits the request to the card brand to debit the cardholder’s account.

- The card brand forwards the request to the cardholder’s issuing bank.

- The issuing bank funds the card brand.

- The card brand funds the processor.

- The processor/acquirer settles the funds to the merchant’s bank minus a “discount rate,” which is the transaction fee for the processor’s services.

- On the cardholder’s end, unlike a typical debit bank account, the cardholder does not receive the debit right away. With credit card transactions, the cardholder’s account will post the transaction, however, they will be billed from their credit card company with their end-of-the-month statement, where they must pay back these borrowed funds promptly to avoid fees.

Do I Need a Payment Processor?

Unless you accept only cash or check, you will need a payment processor. Most merchants today accept credit and debit cards. And if you’re looking at being a competitive merchant in your industry, it is in your best interest to implement cashless payments as well.

Customers appreciate having the convenience of paying with their cards. Many in fact, don’t even carry cash or check on their person anymore.

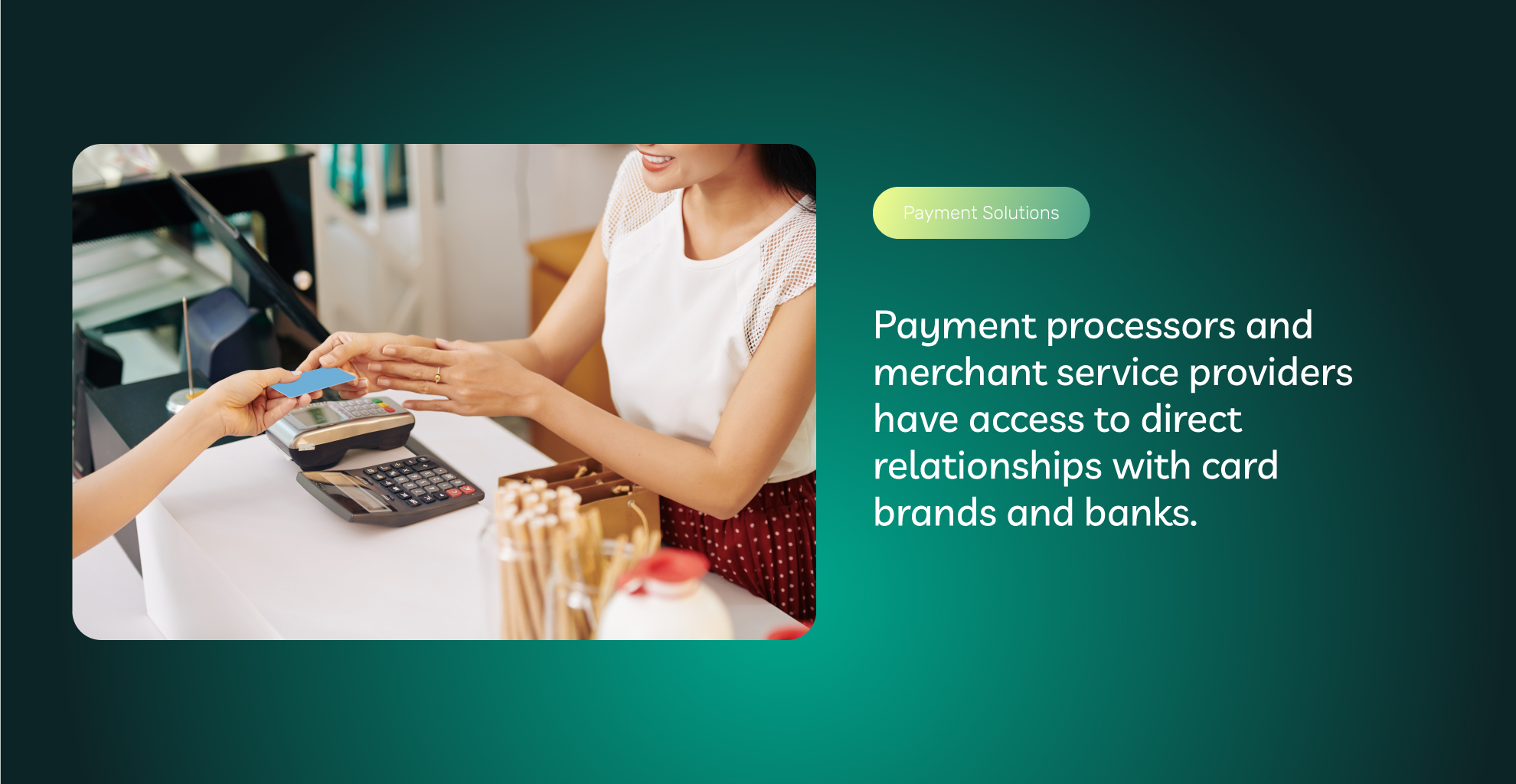

Card brands cannot process card transactions directly with merchants. There needs to be a relationship with a payment processor to connect the two. Payment processors and merchant service providers have access to direct relationships with card brands and banks.

These relationships allow for secure card processing, accurate settlements, and access to customer service that a bank or card network would be unable to provide. Payment processors come in all shapes and sizes. We recommend looking into what your needs are and contacting a few local payment processors for a quote on pricing and solutions.

Security and Regulatory Compliance in Payment Processing

Now that we have gone over the key players involved in payment processing and the process every transaction goes through to finalize a sale, it is best we now discuss payment processing security and regulatory compliance.

PCI DSS

PCI DSS stands for Payment Card Industry Data Security Standards. The card networks American Express, Discover, Mastercard, and Visa, otherwise known as the PCI Security Standards Council, designed these standardized guidelines and regulations to help protect cardholder information and reduce fraudulent activity in the payment landscape.

Any business, large or small that accepts credit card transactions must adhere to these 12 guidelines. Failure to become or remain compliant can result in negative consequences. Such consequences include:

- Fraudulent transactions

- Chargebacks

- Legal issues

- Merchant account closures

- Additional avoidable fees and fines

- The loss of customer trust

- A struggling business or the need to close

The regulations that merchants must adhere to include:

- Using firewalls

- Tokenizing stored card data

- Encrypting sent card data

- Securely storing passwords

- Using anti-virus software

- Taking all measures to keep sensitive information private

- Physically securing stored data

- Keeping all software up to date

- Keeping access logs

- Using unique credential identifiers

- Implementing limited access to sensitive data

- Creating and maintaining workflows and procedures

- Running regular tests and scans

- Using unique passwords

- Updating passwords regularly

So, how do merchants become PCI compliant? Implementing some of these regulation responses might be easy to do on your own daily. However, others, like encrypting data and testing your systems, might prove to be a little more challenging for a non-tech-savvy person.

You may need to look into a dedicated IT team to monitor your systems. Additionally, the right payment processor, like ECS Payments, offers payment solutions with integrated security features such as encryption and tokenization. We also outline the steps and direct you to the right team to help you become PCI-compliant.

Payment Processing Conclusion

The world of credit card processing is more than just your customer’s card, the bank, and the POS device. Just think how involved those 3 little seconds were for you to ultimately make your living, and just how many players were involved in that seemingly quick and easy process. If you want your customers to have ease of transactional accessibility at your business, you will need to accept all types of payment methods, including card payments.

To accept card payments, a payment processing company will be essential to your business endeavor. Some companies, like US Alliance Group Inc., can combine payment processing services in addition to supplying hardware and software like card terminals and online gateways, catering to a well-rounded and efficient experience empowering your business to thrive.

To contact sales, click HERE. And to learn more about ECS Payment Processing visit Payment Gateways.

Updated January 2024