Understanding the principles of accounting is essential for maintaining a company’s balance sheet, which is a snapshot of its financial health. However, there is not one monolithic basic accounting principle for businesses. Several different modalities allow controllers to emphasize assets or liabilities based on which method they choose, for instance, the cash principle versus the accrual principle in accounting.

Most consumers are only familiar with the cash principle, which constructs a balance sheet only from “settled” assets and liabilities. This is the method used on their bank statement: $40 went to lunch, $50 went to a credit card payment, and $500 was deposited into their checking account, resulting in a net sum of $410. For now, at least.

But does this type of financial accounting basics accurately portray their financial health? Accounting principles and business success often demand a different outlook. For instance, suppose that same consumer actually has an annual salary of $80,000 and net annual expenses of $70,000. The resultant $10,000 on the books looks a lot different than $410, particularly to a lender.

That’s the importance of accounting principles that offer more flexibility. Now imagine that we aren’t looking at a consumer but rather a business enterprise with much larger expenses and much more revenue. They want to minimize their tax burden while also maximizing the appearance of their profits for investors. Can they do both?

Let’s take a look at some accounting principles that have been explained.

1. The Accrual Principle: Recognizing Revenue and Expenses

The accrual principle is a time based accounting method. This means that revenue and expenses are recognized when they occur. Sales are recorded when goods are provided or services are rendered, not when the customer or client pays, even if they can enjoy delayed payment arrangements like Net30 or 2/10. Sometimes, this is called the revenue recognition principle.

Expenses are also recorded when they are used or enjoyed, not when payment is made. For instance, if a company hires a consulting firm for a week long review but agrees to a 12 month installment plan to settle the balance, the expense will still be recorded at the end of the week.

Don’t count your chickens until they hatch, the old adage goes. Why on earth would you count them until they’re chirping? It’s always possible for eggs to fall and crack. While it’s true that cash settlements offer a degree of finality, waiting until cash is “in hand” (or out of your hands) does not necessarily create an accurate financial picture of your business.

Examples of the Accrual Principle in Action

Take both of the examples mentioned above. Suppose you sell $100,000 worth of goods to a customer but give them Net90 arrangements since they’re creditworthy. If you’re trying to forecast your finances and make some decisions over the next three months, you should make them knowing that you essentially have $100,000 additional funds to play with.

On the other hand, suppose you hire that consulting firm for a week long observation. Although you don’t pay them $20,000 upfront, you will be out twenty thousand dollars over the next year (if you have a 12 month payment plan). That should also factor into your business decision making process.

Bringing both these examples together, the sales and expenses balance out to an $80,000 surplus. No, it’s not in your hands yet, but it’s reasonable to rely on the likelihood that it will be. This is why the accrual principle is often viewed as providing a more accurate, real time picture of a company’s actual financial health.

An additional benefit to the accrual principle is that expenses are recorded in their actual time frame. Recording expenses (and revenue) as they occur can also make it easier to stay compliant and to strategize tax returns. For instance, suppose that the consulting visit began on December 29th or that those Net30 goods were sold before January 1st. The accrual principle would allow you to capture these gains or losses on that year’s tax return.

Challenges of the Accrual Principle

The accrual principle has some downsides. It can create an inaccurate view of a company’s immediate cash flow. Because it records expenses before they’re finalized, it can involve more labor and detail in record keeping. There is also greater room for subjectivity and occasionally even fraud.

For instance, an accountant could record the $100,000 in profits from our above example while hiding the $20,000 consulting fee. Or, they could record the $20,000 consulting fee as a business expense and hide the six figures in revenue to decrease their tax burden. One obvious way to prevent this “poetic license” is to implement strict controls that require consistency in accounting methods across the board.

2. The Consistency Principle: Maintaining Uniform Practices

That’s where the consistency principle comes into play. There are other accounting methods aside from the accrual method, like the cash method. As mentioned, this method records expenses and revenue only after transactions are finalized. Then, there are ways of accounting for inventory: FIFO (first in, first out) and LIFO (last in, first out).

These various methods all fall within the scope of Generally Accepted Accounting Principles (GAAP). The purpose of GAAP is to make financial statements consistent, comparable to others, and transparent. This information is important for investors and creditors to make informed decisions about buying shares (of publicly traded companies) or lending.

A Lesson from Enron: The Cost of Inconsistency

One of the most infamous examples of a business violating the consistency principle was Enron and its accounting firm, Arthur Anderson. AA (not to be confused with the airline or the 12 step program) used a variety of accounting methods to emphasize certain numbers while hiding others. They even created special purpose entities (SPEs) off the balance sheet to hide debt and inflate earrings.

The SEC slapped Arthur Anderson with $10 million in fines, and some of its executives went to jail. Enron went bankrupt, although apparently (going by social media posts), they’re back (we’ll see how things go this time around).

Using different accounting methods isn’t necessarily illegal, but these differences must be disclosed. This information should be placed in footnotes to company financial statements. In annual reports, detailed disclosures should be placed, particularly in the MD&A (Management’s Disclosure and Analysis). Other SEC and tax forms must be filled out to disclose different accounting methods.

If this isn’t giving you a headache, it should be. Varying your accounting methods is complicated and fraught with legal pitfalls. For most SMBs, it’s far better to stick with one accounting method.

As it turns out, the best method for most startups in the Shopify phase of life is the cash method. The accrual principle has its merits, but (as mentioned) it is a little more complicated. And yet, once a business reaches a more normal industry sales volume, switching to an accrual principle may be beneficial.

FIFO, LIFO, and COGS

Let’s circle back to FIFO and LIFO vis-a-vis the consistency principle. FIFO and LIFO are inventory valuation methods. As mentioned, FIFO stands for first in, first out. It’s an accounting method that assumes the oldest inventory is sold first. LIFO stands for last in, first out. It’s an accounting method that assumes the freshest inventory is sold first.

Businesses with inventory that consistently rises in price will often use the LIFO method. Retailers, car dealers, electronics vendors, and manufacturers often use the LIFO method because it allows them to match up the recent (and probably highest) costs of goods sold (COGS) with their revenue. Businesses with perishable inventory, such as restaurants, pharmacies, grocery stores, and seasonal retailers, often use the FIFO method.

For instance, suppose an electronics vendor pays $100,000 for a shipment of kitchen appliances. Six months ago, they paid $80,000 for the same shipment (prices rose 25%). Let’s say they sold one round of inventory for $200,000.

Using the LIFO method:

They’d subtract $100,000 (rather than $80,000) from the sales, yielding $100,000 in profits. This number, less than $120,000 (had the $80K been subtracted), looks like less revenue, but it also means less of a tax burden.

Using the FIFO method:

Let’s suppose that the same business is trying to look attractive to a lender or outside investor. They’d have to unload the oldest batch of inventory from the balance sheet first rather than the most recent. That means holding up the $80,000 COGS against the $200,000 profit for a net $120,000 gain. More taxes and more revenue are needed, which looks appealing to investors or lenders.

As you can see, each situation has its merits. The problem is that a business cannot use FIFO for some inventory and LIFO for others. In this case, the consistency principle is a mandatory reporting requirement that keeps inventory valuation transparent.

Also, keep in mind that we are discussing FIFO and LIFO from the perspective of the “balance sheet.” This balance sheet is a snapshot of how things are going “currently.” The fact that there is a “current” accounting period to discuss implies that there is some business continuity and that there will be other “current” periods in the future.

3. The Going Concern Principle: Assuming Business Continuity

The going concern principle assumes that a business will continue its activities indefinitely. This fundamental assumption means that the business will not be liquidating its inventory or ceasing operations. Wondering why that matters?

The assumption that business will continue as usual facilitates some of the accounting principles outlined above, such as the accrual method of accounting. If a business was going to liquidate its assets (in the foreseeable near future), it would not be possible to use more flexible accounting methods that allow a business to record transactions that haven’t settled yet (revenue or expenses).

Of course, the going principle also facilitates investment and lending. Generally speaking, consumers and investors are not interested in investing in a business that won’t last, and lenders are not interested in extending credit to such a business.

The going principle allows a business to invest in long term assets that can be paid off over time. Businesses can forecast and model future financial performance and create a plan for paying down debt. They can also leverage long term tax strategies like depreciation.

For instance, a business or investor can often depreciate commercial property over 39 years (27.5 for residential property). This means they can spread the cost of this property out over 39 years, subtracting it as an operating expense for tax purposes.

Why These Principles Matter to Business Leaders

Accounting principles and financial decision making go hand-in-hand. Core principles of accounting allow for more flexibility in financial management. As mentioned, accounting methods (can), for example, influence the look of statements.

Do you want the balance sheet to reflect more revenue, making greater appeal to lenders and investors? Or would you prefer the balance sheet to reflect more expenses, reflecting a lower tax burden? You can have your cake and eat it, too, as long as you are doing everything legally.

However, a basic principle for controllers is not to eat more than you can lift, as Miss Piggy famously said. Do not try to juggle too many different accounting methods on your own. As mentioned, varying your methods will require forms and disclosures, not to mention the fact that you usually cannot use FIFO and LIFO methods of inventory valuation simultaneously.

Simplified Accounting for Small Businesses

Small business accounting tips should be geared towards simplicity unless you have the resources to adopt more complicated accounting strategies, such as outsourcing your accounting to a firm or hiring an accounting department. However, accounting principles for small business owners will also depend on broader industry and market factors. Let’s take a look at FIFO and LIFO, for example.

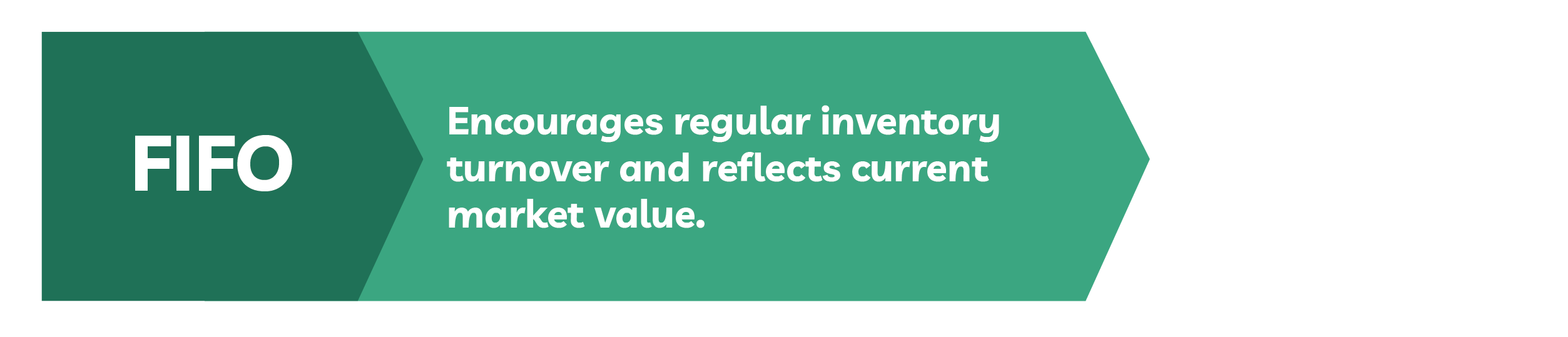

FIFO: First In, First Out

FIFO encourages regular inventory turnover, as the name implies: first in, first out. Because later inventory often is subjected to rising prices, the FIFO method tends to leave a higher revenue on the balance sheet. Since the remaining inventory is contemporary with current prices, it also provides a more current market value of said inventory.

There are a few cons to FIFO. One is (as mentioned) more income to report for taxes. This, however, can potentially be mitigated with losses and tax write offs. Another con is that FIFO can be troublesome for businesses with stagnant inventory. For these reasons, businesses with slow moving inventory like machines or electronics might stay away from the FIFO method.

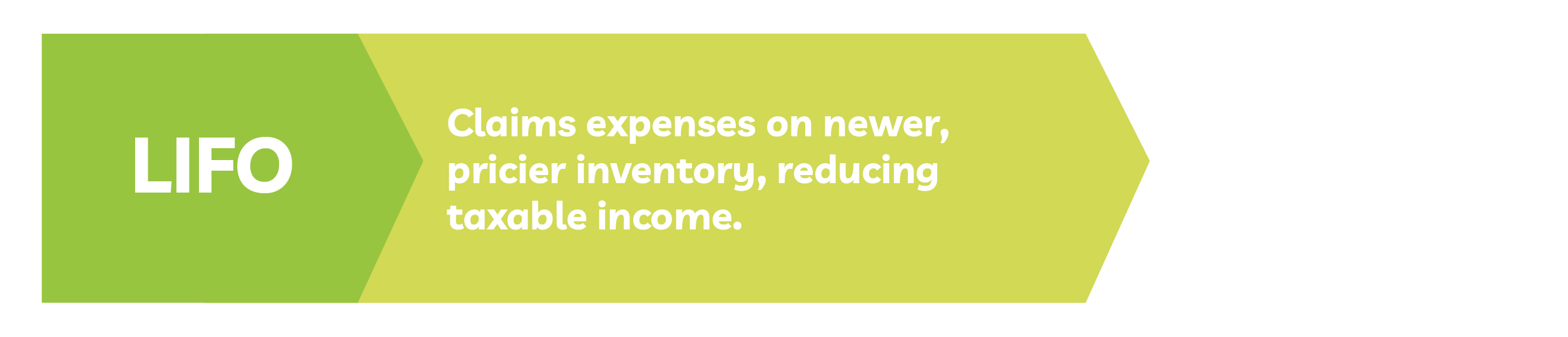

LIFO: Last In, First Out

LIFO does not necessarily encourage regular inventory turnover as much as FIFO and older inventory can stagnate. That might be okay if the older inventory is dumped as a write off or sold on a secondary market.

Some retailers do this by dumping inventory into a network of retail outlets. LIFO does allow a business to claim more expenses, as more recent inventory tends to be more expensive. Real estate investors would certainly find LIFO more appealing.

Cons to LIFO include a slightly less accurate representation of your inventory flow. It is also not an acceptable accounting method in every jurisdiction. While it’s legal inside the United States, it’s illegal in many other places internationally, at least the ones adhering to the International Financial Reporting Standards (IFRS). For these reasons, international businesses will probably need to avoid the LIFO accounting method.

Implementing Core Principles in Day to Day Business Operations

How can these accounting principles for controllers be upheld? How can accounting compliance guidelines be adhered to? It helps to have a competent accountant or accounting department. Many businesses, even corporations, outsource their accounting to a third party. These third parties are responsible for preparing financial statements and filing income taxes.

However, the business still has the responsibility to accurately record its expenses and revenue in every reporting period. This is easiest when accounting systems are integrated with the point of sale and payment gateways. It’s also possible to ensure that all software adheres to the Financial Accounting Standards Board (FASB) in terms of how expenses and revenue are recorded.

The bottom line is that maintaining compliance and consistency in accounting practices is best achieved when more functionalities are automated. It also becomes easier to compare financials between periods and adjust tax strategies accordingly. These days, it is more than possible to integrate multiple systems for immediate and accurate recording and reporting.

Conclusion

Accounting principles for leadership of a robust and compliant company are built on the accrual principle, the consistency principle, and the going concern principle. When a business is first starting out, there is not much need for complicated accounting methods beyond immediately recognizing settled revenue and settled expenses.

Employing an accrual method of accounting allows for greater flexibility in determining whether a business should emphasize assets or liabilities. Cash flow and assets are key to appealing to investors, but reducing tax burdens requires emphasizing liabilities.

Competent accounting will employ legal strategies to crunch the numbers in the best way possible for your business. Integrating accounting software with the point of sale can remove a lot of the legwork. Accounting suites can also contain industry and state specific legal parameters to stay compliant automatically.

Frequently Asked Questions About The Principles of Accounting

The cash method records revenue and expenses only when money changes hands, which is great for simplicity. The accrual method is more comprehensive, it recognizes revenue and expenses as they occur, regardless of when payment is made. While cash based accounting is easy to follow, the accrual method gives a more accurate snapshot of a business’s financial health by reflecting obligations that have yet to be paid.

Cash accounting is often the simplest and most effective method for small businesses. It’s straightforward and aligns with how most people think about their personal finances: recording transactions when money enters or leaves your account. However, transitioning to the accrual method as a business grows might offer more accurate insights into long term financial health and provide greater flexibility for tax planning and investment decisions.

The consistency principle ensures businesses use the same accounting methods consistently (if the name didn’t already suggest that). It provides clarity, comparability, and more informed decisions. Without consistency, companies could manipulate financial statements by choosing methods that highlight certain numbers to their advantage.

FIFO (First In, First Out) assumes the oldest inventory is sold first, it offers a more accurate reflection of the current value of your inventory and can be beneficial for companies with fast moving or perishable goods, which can lead to higher reported profits if prices are rising.

The going concern principle assumes that a business will continue to operate indefinitely. It allows businesses to plan long term, make investments, and use accounting methods like accrual accounting.