Merchant pricing models, even the best ones, mean that you will pay to accept credit cards. Sometimes, there is no way to achieve a good payment processing cost reduction. In these cases, reducing credit card processing fees with dual pricing implementation might benefit your business. Let’s take a look at dual pricing and the legal considerations of dual pricing.

Understanding Dual Pricing

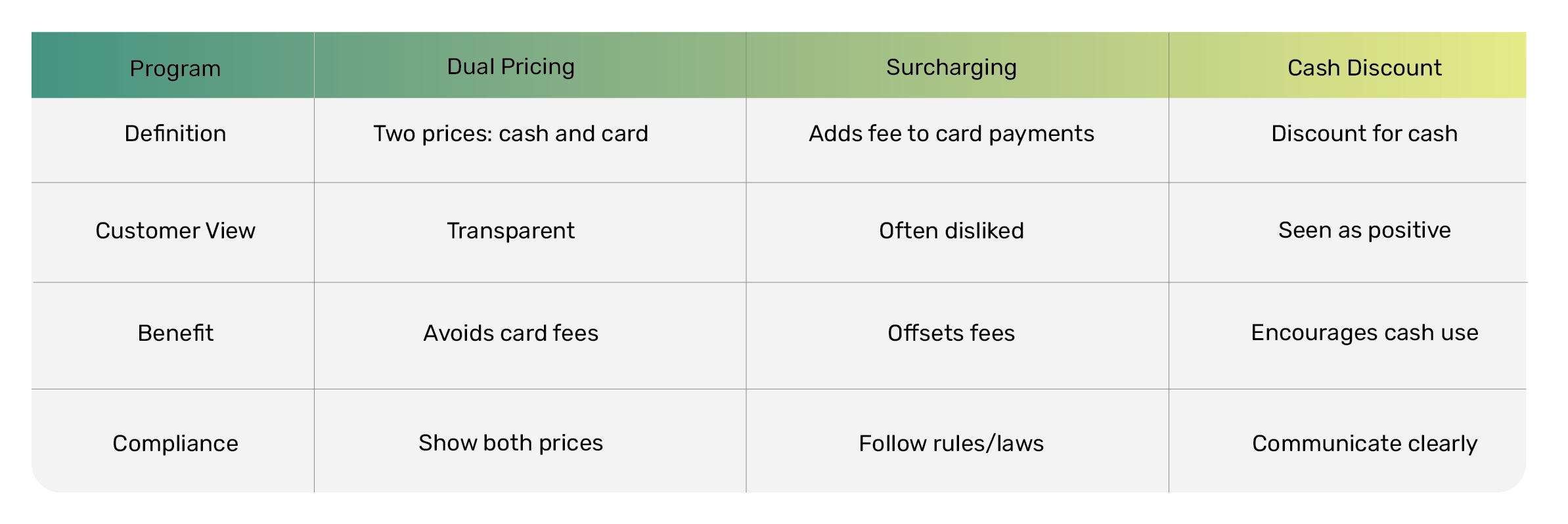

Dual pricing is another name for cash discounts. The purpose of dual pricing—or cash discounts—is to encourage customers and clients to pay with cash, debit cards, or checks instead of credit cards.

Keep in mind that if your payment processor charges one flat fee for all card types (debit and credit), cash discounts should not include debit cards. If your bank charges a flat fee to deposit a check, it could still make sense to offer cash discounts—because a flat fee will still be lower than a percentage for large purchases.

Surcharging is not the same as a cash discount, even if it has the same underlying purpose. A surcharge is a fee—a flat rate or percentage fee—applied to credit card purchases. Surcharges are often conflated with convenience fees, but a convenience fee is a different type of charge—it’s meant to cover the cost of accepting payments through alternative channels online or over the phone.

In summary, dual pricing (cash discounts) and surcharges both aim to avoid payment processing costs. A cash discount seeks to avoid the cost entirely by encouraging non-credit payments to avoid the fees. A surcharge seeks to avoid the cost by having the customer cover the payment processing fees.

Benefits of Dual Pricing for Businesses to Reduce Credit Card Processing Fees

The obvious benefit to dual pricing is that you will avoid credit card processing fees without having to employ the ugly word “surcharge.” Customers usually hate having to pay additional and/or “hidden” fees. Even if you have signage at the point of sale and on receipts (as required by Visa and Mastercard for surcharges), customers do not usually expect to pay 3% more on their purchase.

Dual pricing also encourages cash payments. Generally speaking, credit card settlements don’t take that long, but nothing beats cash in hand. Sometimes, a small business wants customers who pay now and want to be able to take that money to the bank the same day. Credit and debit cards can’t help as much as cash.

Dual pricing—by eliminating credit card fees—can also improve your profit margin. You just have to make sure the cash discount does not exceed your credit card payment processing fees. For instance, if your payment processing fees are 2.6% of every transaction, you would not want your cash discount to exceed 2.5%. Otherwise, dual pricing becomes “six of one, half a dozen than the other.”

Dual pricing, when employed strategically, can also boost sales volume. Advertising cash discounts can make it seem like you’re having a sale or reducing the price of inventory, even if that’s not the case.

Challenges of Dual Pricing

Dual pricing has drawbacks, and we would be remiss not to mention them. However, for each drawback, your payment processor can offer a solution or that you can implement with customer-facing best practices.

One immediate issue is the extra layer of complexity demanded by offering dual pricing models. If your cashiers need to compute the discount manually, that will create a quagmire at the point of sale. Of course, an easy way to deal with this issue is to automate the process with the help of your payment processor.

Another issue is the price discrepancy that is evident to customers. Customers with credit cards may feel penalized. It’s evident to them that you are trying to avoid credit card processing costs. However, these negative sentiments are more pronounced when using a surcharge instead of dual pricing or cash discounts.

Think of it from the customer’s perspective: if pricing is the same for everyone, but American Express holders need to pay an additional 3%, cardholders of that particular card will feel persecuted. On the other hand, with dual pricing or cash discount, you are not slapping on extra fees…you are just reducing them for customers who choose to pay with cash, check, or possibly a debit card.

However, you should still keep in mind that to some customers, a discount for others is the same as an additional fee for them. Dual pricing is not as bad as a surcharge in this regard, but it can still leave a bad taste in their mouths.

Legal and Compliance Considerations

According to the Constitution, surcharge programs and dual pricing or cash discounts are federally protected rights. That may surprise you because they’re not particularly enshrined in the ConstitutionConstitution next to things like 2A. However, numerous court cases have established that they do fall under the right of free speech, or the First Amendment.

That is to say, merchants are free to advertise prices as they see fit, which can include surcharging or discounts to cover or avoid the cost of processing payments. Legally, this is also not a form of discrimination, because consumers still have a choice to pay with cash.

However, just because something is permissible at the federal level does not mean there aren’t regulations within every state. Moreover, Visa and MasterCard also have rules about how you are allowed to surcharge and offer dual pricing. If these rules are not followed, you run the risk of being blacklisted by these card networks…and then you’ll be an all-cash business.

Implementing Dual Pricing in Your Business To Reduce Credit Card Processing Fees

First, you must figure out how much your cash discount should be. That will involve discussing your credit card processing fees with your payment processor. If you are subject to flat-rate processing fees, this will be easy to figure out. Incidentally, however, if you are paying flat-rate fees, there is another conversation you should have: figuring out how to switch to interchange rates plus markup pricing (but that’s a story for a different day).

Cash Discount Programs with Interchange Plus Pricing

If you already enjoy the benefits of interchange plus pricing, cash discounts could be a little trickier because every transaction has a different cost. Your payment processor can give you a breakdown of the most common card types. From there, you can either take an average of the fees or match the discount to the fee for one particular card.

Don’t jump the gun and assume you should match the price to the most expensive card. You may want to take a more nuanced approach and see what cards are typically used for the largest transactions. If you have a mix of consumer and business clients, for instance, your business cards, such as American Express, will have higher fees.

You may want to match your cash discounts to these cards instead of offering them to a more frequently used card, especially if the ticket sizes paid for with those cards are much smaller. This is a very nuanced goal that can only be achieved when you can sit down with the payment processor and figure out the hard numbers.

Streamlining the Checkout Process

Next, we need to figure out how to implement this cash discount at the register. Thankfully, the payment processor can take on this task for you. The most up-to-date POS hardware connects to phones or tablets that can provide a touchpad interface at the point of sale. This means that cashiers can just push a button at the time of a transaction to implement a cash discount.

No more brow-scrunching and mental gymnastics to slow down the line of customers. What about B2B payments online, like invoices? For invoicing, if you are providing cash discounts for debit cards, the discount can be applied through the payment gateway.

The Benefits of ACH Payments

If you have a subscription-based business or one where customers are periodically charged, you may consider emphasizing ACH payment options and enticing customers toward them with a cash discount.

ACH payments take funds directly from the customer’s bank and deposit them into yours through the automated clearing house network. No card networks are involved, which means you significantly reduce credit card processing fees.

Most ACH payments take just a handful of dimes to process at most. While this doesn’t make sense for low-ticket, high-volume sales, it makes a lot of sense if you are collecting large payments like rent, tuition, or expensive business software licensing fees.

ACH payments are extremely easy to set up, and your payment processor can help facilitate that. All that’s typically needed from the customer is their banking information, account and routing number, name, and possibly a few other pieces of information, such as their address.

ACH payments are cumbersome to implement in a store, as a customer will have to hunt for their checking account and routing numbers on a check or in their banking app. However, you can also Collect ACH payments over the phone as long as you adhere to state rules.

Usually, these require reading a brief disclosure. No matter how the ACH payment is collected, over the phone, online, or in person, an agreement must be signed with the customer about the amount and day of the payment moving forward.

Communicating Dual Pricing to Customers

Now, let’s discuss how you communicate dual pricing to customers. If you have a brick-and-mortar store, clear signage should be placed at the point of sale. This signage should look professional rather than handwritten.

A plaque on the wall or on the counter with a clean font goes a long way. If your corporate style guides permit, adding a graphic or whimsical touch can also smooth the waters a bit.

When cash discounts are applied, the discount should be displayed on the receipt, including the percentage and the resulting dollar amount. Again, this will require a conversation with your payment processor about automating the application of set discounts.

Much of what we said about dual pricing has, to a slight degree, involved shying away from advertising these discounts prominently (other than the issue of transparent signage at the point of sale).

However, sometimes you may want to celebrate your cash discounts. You can make cash discounting part of the marketing campaign. You may want to weigh the pros and cons of increasing the discount for a certain period, as it may appear punitive to customers who want to pay with a card.

For instance, if your usual dual pricing offers a 2.5% cash discount, “combining” it with a seasonal promotion for a 5% cash discount could have pros and cons. In some states, this may also be illegal.

Challenges of Implementing Cash Discounts

Cash discounts are not easy to implement in every type of business. Businesses with a high sales volume and rapid-fire sales may find them difficult to implement because most consumers don’t carry cash. However, if your payment processor can assist and implement a cash discount with debit cards, that may help you achieve some cost-effective savings.

Earlier, we mentioned that even though dual discounting does not seem as punitive as surcharging, it can still leave a bad taste in some customers’ mouths. One way to get around this is to situate cash discounting within the context of other discount options, such as a loyalty rewards program.

Consider Loyalty Programs

If customers and clients see a cash discount as just one of the discounts you offer in tandem with others, it will be more palatable. Loyalty programs are also a great way to reduce churn and increase customer lifetime value, often immediately increasing average ticket sizes.

Your payment processor can also help you implement a loyalty rewards program, using the point of sale as a check-in and integrating with your CRM. The loyalty program will be automated, so you do not need to use old-school manual methods like punch cards or stamps.

While consumers may balk at the idea of surcharges or cash discounts, most B2B clients are understanding. They are already familiar with payment terms that encourage early payment, such as 2/10 (a 2% discount is applied if full payment is made within 10 days, as opposed to the usual arrangements like net-30).

Business owners typically like to have net 30 arrangements so they can recoup the profits on inventory before paying for site inventory. However, business owners also like to save money, and sometimes, there will be periods when they actually have the cash in hand, such as after a seasonal burst like the holidays.

Monitoring and Evaluating Dual Pricing Effectiveness

It’s never a good idea to implement something in business and let it continue forever without checking on it. Thankfully, the point of sale becomes a gateway for examining vast amounts of data. Once you implement cash discounts, your payment processor can help you see if they are working.

You’ll be able to examine new data points, such as transaction volume by week, day, and even time. You’ll be able to see what types of cards consumers are using, such as debit or credit. And you’ll be able to see if the average ticket size has changed. Studies have shown that consumers using credit cards tend to make larger purchases, which is another drawback to incentivizing cash usage.

When you have the data, you can examine all of these considerations around a dual pricing strategy. Your payment processing software can also help ensure you are staying abreast of Visa and Mastercard’s dual pricing compliance (e.g., displaying the percentage and discounted cash amount on receipts).

Conclusion In How To Reduce Credit Card Processing Fees

Let’s recap dual pricing for small businesses. Dual pricing is also referred to as a cash discount. Dual pricing vs. surcharging is different, as surcharging means adding a fee to credit card (possibly debit card) sales. However, the end goal is the same: avoiding credit card fees.

There is no need to purchase a special dual pricing point-of-sale system. Your payment processor can help implement a dual pricing program, and observe dual pricing impact on sales. You do want to offer robust and proactive customer communication for dual pricing, and at times you may even want to flaunt it (as a sale).

Dual pricing best practices are best worked out with your payment processor. They are often difficult to implement manually (e.g., calculating the discount at the time of sale). Moreover, manually applying the discounts can violate the consistency and receipt-based verbiage that card networks request.

Frequently Asked Questions About Reducing Credit Card Processing Fees With Dual Pricing

Dual pricing is a term for businesses that offer a different or lower price when customers choose to use cash, debit cards, or checks instead of credit cards.

Dual pricing reduces credit card processing fees by encouraging non-credit payments. A business’s regular price accounts for credit card processing fees, saving money, but customers paying with non-credit methods avoid those fees, saving them money. In short, dual fees increase a business’s profit margin.

Yes, dual pricing is legal at the federal level under free speech rights. However, state laws and card network rules may impose specific requirements, such as signage and receipt disclosures.

With your payment processor’s help, you can automate dual pricing. Updated POS systems can apply discounts automatically, ensuring a smooth process for cashiers and customers at the point of sale.

Use clear, professional signage to explain dual pricing at the point of sale. Ensure receipts display the discount and its calculation transparently. You can even promote cash discounts as part of your marketing strategy to attract customers.