Business owners are feeling the pinch, but aren’t they always? When your goal is to keep more of the money you make, you’re always looking for ways to save and avoid hidden fees. One of the first things small businesses look at is their human capital costs. Can we cut hours? Fire anybody? A second place they look is in retail-related overhead. Perhaps we can move to a different location?

These options could help but, sometimes they have disastrous consequences. SMBs are better off looking for ways to trim their business process operating expenses. One easy way to save for some merchants might be to reduce credit card processing costs. And one way to do this is to consider pass-through fees.

Have you ever examined your merchant service fees? Understanding credit card statements and their fees can be the gateway to saving a few percentage points of your losses every year. You may be paying hidden credit card fees you never knew about…until now.

It’s time to get transparent about payment processing. Let’s talk about the benefits of pass-through pricing.

What is a Pass-Through Fee?

Many smaller businesses will use flat-rate credit card processing or bundled pricing as an easy go-to processing model. However, some businesses have learned to use pass-through payment processing pricing models to manage the cost of transactions processed.

We’ll talk about flat-rate pricing in a little bit. Suffice it to say (for now) that every transaction gets hit by the exact same fee, regardless of what card a customer uses. In a bundled pricing model, you’ll pay one flat fee every month to run as many transactions as you’d like, up to a certain amount.

Sounds like a great deal…if you’re talking about a buffet. But when it comes to payment processing fees, this is a bad arrangement. Chances are you’ll have a variegated sales volume. What happens during the months when you’re far below your limit? Will your transactions roll over to next month?

We can’t spell out the nuances of every potential bundled pricing contract. However, generally speaking, bundled pricing for credit and debit card transactions is not beneficial for the merchant. If you end up selling more products or services, you’ll undoubtedly have to pay additional fees for every transaction.

The best type of fee for accepting credit card payments is pass-through pricing. As the name implies, the costs are passed on to you. But that’s not a bad thing. With other pricing schemes, you’d be paying them anyway…and more in hidden fees. As you’ll see, pass-through pricing is a much more transparent arrangement with your credit card processor.

Types of Pass-Through Fees

Let’s break down merchant account pass-through fees. There are three main components: interchange fees, assessment fees, and markup fees. Each fee is charged by one of the many parties involved in a card transaction.

First up, we have the interchange fees. These fees are charged by the card network that carries the transaction. They charge the credit card issuer (e.g., the customer’s bank or credit card company). A few factors impact the exact cost of this fee, including the type of card (credit, debit), the size of the transaction, the nature of the transaction (in-person versus online), and your Merchant Category Code (MCC).

An MCC defines the primary business activity of your organization. There are thousands of MCCs that banks and card networks assign to businesses. It’s tough to change your MCC once it’s assigned the first time you apply for merchant services. If you’re in the startup phase, make sure you clearly and accurately describe your business objectives when applying for merchant services or payment processing!

Next up, we have assessment fees. The card network also issues these fees to help cover their operating expenses. If you’re wondering what expenses Visa, Mastercard, Amex, and Discover could possibly incur, think of things like fraud prevention, customer service, marketing, and even credit card rewards. The assessment fees are often charged to the issuing bank as well, which passes them on to the merchant.

Finally, we have the processor markups. Your payment processor charges these fees to cover their operating expenses. Just like the card networks, they, too, must provide fraud protection and customer support. They have payroll and marketing expenses, and often, they also must provide and service the hardware they are leasing to their customers (like you).

Understanding Credit Card Processing Pricing Models

Aside from bundled pricing, let’s examine some of the more common pricing models that different types of businesses are subjected to.

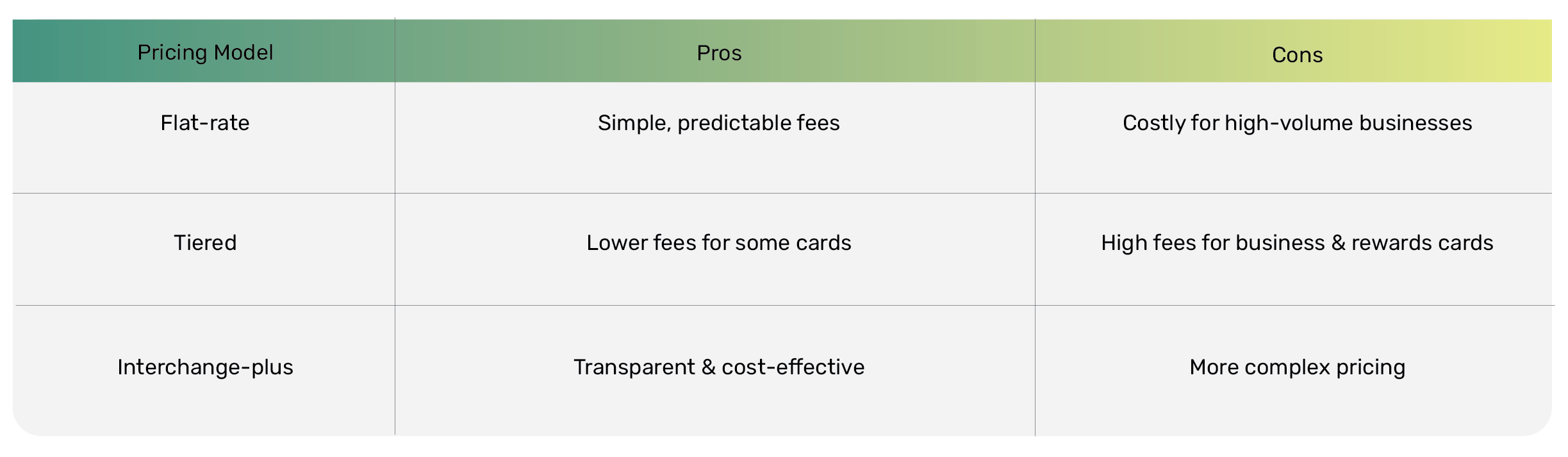

Flat-rate Pricing

Flat rate pricing is one of the most common pricing models encountered by small businesses—particularly in the startup phase. As the name implies, every transaction is charged the same fee. Companies like PayPal, Square, Stripe, and Clover typically apply flat-rate processing to their merchant customers.

Usually, these credit card processing fees hover between 2.5% to 4% plus change for every transaction. If you’re even a little good with numbers, you know this will shave a decent chunk off your earnings. To be fair, some may offer improved pricing once the sales volume increases beyond a certain threshold.

However, it will still be a “flat rate” in the sense that every transaction will be subject to the same fees. Many SMBs eyeball this discount and assume they are getting a good deal…after all, what’s not to like about fees dropping half a percentage point?

What’s not to like is the fact that, in truth, every type of credit card or debit card has a different cost when running through the networks. Flat rate pricing does not reflect these differences, and the one paying the difference is the merchant.

This doesn’t matter to a Shopify merchant selling homemade soap out of their garage. But what happens once they start selling 10,000 bars of soap a week? Or 100,000? Flat rate pricing could cost them tens of thousands of dollars every year.

Tiered Pricing

Another seemingly more nuanced option is tiered pricing. Typically, tiered pricing places cards into three categories: qualified, mid-qualified, and non-qualified. In truth, these applications refer to the amount of risk each card presents to the payment processor or financial institution providing merchant services for business.

For example, debit cards fall into the qualified category, which will have the lowest fees. Business cards and high-reward credit cards often go into the non-qualified category. Cards in this category are viewed as being more often subjected to fraud, disputes, and chargebacks. As such, they present a greater risk to the payment processor.

The merchant services provider will charge higher fees for these transactions to cover their risk. Unfortunately, some of the best business comes from rewards and business credit cards. These cards are often used to make larger purchases, either because the purchases are incentivized or because the purchaser is placing a large order.

Can you see where this is going? All of your best business is going to be subject to higher fees. Consider this with credit card fees: tiered pricing is all about hedging risk for the payment processor.

Interchange-plus Pricing

Interchange plus pricing is truly the best fee model for most businesses. It is also the most transparent model because the payment processor acknowledges the true cost of running a transaction and then adds their fees on top of it, in contrast to hiding their own potential savings behind a flat fee.

This pricing model’s “interchange” component refers to the cost of running the card through card networks Visa, MasterCard, AMEX, and Discover. The “plus” component—also called markup—is the fee the payment processor adds to cover their own costs.

Why Pass-Through Fees Are Charged

The first thing you have to understand is that unlike exchanging cash or even an ACH transfer, credit and debit card transactions involve multiple parties: the customer’s bank, the card network, and your bank. Then there’s the frontline party that facilities all of the above by providing the hardware and software for taking credit cards: your payment processor.

Everybody wants a slice of the pie, and they deserve it as well. Each party plays a vital role in moving the money from your customer’s bank account to yours. Without them, you could not be collecting payments. Like any other business service, they are going to charge you.

Of course, the question is how much they should charge. Much of that has to do with the type of business you run (your MCC code), the transaction’s size, and the transaction’s nature. For instance, card-not-present transactions are more likely to become subject to fraud. With more risk, the credit card interchange fees need to be higher. Think of it like your insurance premiums: your rates will be higher if you drive a red sports car.

It’s hard to think of a reason why Visa or Mastercard should eat the fees it takes to run card transactions. In fact, this is really their only source of revenue. The same is true of your payment processor. While you obtain revenue from selling goods or services, their service is helping you process card payments.

However, if you pick the wrong pricing model, you’ll pay more than you should. If you’re using a company like PayPal, Stripe, or Square, you might be paying them much more than necessary to cover their operating expenses. That’s why you should re-evaluate interchange fees vs. tiered pricing vs. flat rate pricing schemes.

How to Identify Pass-Through Fees on Your Statements

Now that you’ve become aware of the different types of fees, how can you identify them in your statements? If your payment processor charges you a flat rate or a bundled fee, good luck breaking down the numbers behind the fee! However, if you’ve got a pass-through rate, here’s what to look for on your statement:

Interchange fees, assessment fees, and markup fees should be listed separately. Be on the lookout for additional verbiage like monthly minimum fees, chargeback fees, and international fees. If you don’t know what type of credit card assessment fee you’re looking at, ask! Your payment processor should explain all interchange and markup fees.

Benefits of Pass-Through Fee Pricing

Let’s look at some of the benefits of pass-through fee pricing.

First off, there is a much greater degree of transparency. You will see the true cost of the transaction right in front of your eyes instead of having it hidden behind something like “2.5% + 30 cents for every transaction!”

The next immediate benefit is the obvious cost savings. The true cost of a transaction is often far below the “industry standard” of flat fees charged by Venmo, Shopify, or PayPal. As mentioned, the savings are even greater than bundled pricing, when you could pay for a lot more than you’re taking.

Another benefit is that you can sometimes negotiate the markup fees with the payment processor. As your business grows, they’ll be making more money off your cash flow, and you can use that to your advantage to negotiate lower markups.

Drawbacks of Pass-Through Fee Pricing

There are some “drawbacks” to pass-through pricing. Obviously, the pricing structure is more complex. Your bill will have a lot more bells and whistles. In rare instances, the true cost of running a transaction (cough cough, Amex) will be higher than the “industry standard” of cookie-cutter online payment gateways.

To be fair, the simplicity of flare-rate pricing is a selling point for merchants with a low sales volume, who are just starting out. Since their sales volume is low, the flat-rate pricing might even be comparable to what pass-through pricing would offer anyway (that is to say, the markup would be higher because the payment processor handles fewer transactions).

However, by and large, pass-through pricing schemes are far more advantageous to a business with a “normal” or larger industry sales volume.

How to Minimize Pass-Through Fees

You’re probably wondering if there is a way to lower your pass-through fees. Indeed, there are several. First off, you could negotiate better markup rates with your processor. You can’t obtain that convenience with a flat rate or a tiered pricing model.

More likely, you could manage the types of transactions you take. Ask customers if they are using a debit card so they don’t hit “credit” at the terminal (because there are separate debit card networks, and the interchange fees are lower). Are you having customers scan QR codes to make payments in person? While convenient, these are card-not-present transactions since they’re the same as online purchases (and they’ll cost you more).

Speak to your processor about using Level 2 and 3 data protocols for B2B sales. These involve inputting more information about the buyer, reducing fraud risk. Probably every business taking B2B orders with Stripe terminals or a Clover POS is missing out on this tip…which is only possible when working within the complexity of more nuanced pricing schemes.

Can you issue surcharges to customers using certain credit cards with higher fees, like rewards cards and business cards? You certainly can. It’s legal and federally protected under the First Amendment. However, in most locations, you must post specific signage and language, such as putting the exact dollar amount of the surcharge on the receipt.

Common Myths About Pass-Through Fees

Let’s debunk some common myths about pass-through fees.

“Pass-through fees are the same with every processor.” No, they are most certainly not! Remember that interchange fees are immutable according to the eternal law of Visa and Mastercard, carved in stone (we’re jesting a little bit). However, markup fees only cover the processor’s operating costs.

There are thousands of payment processors, each with differing operating cost levels. Don’t be afraid to shop around and see which processors can offer you a lower markup! Another thing to consider: some payment processors specialize in working with “high-risk” businesses or merchants. If one payment processor is going to charge you too much to cover their risks, find a different one who works with your type of business.

“Interchange fees can be negotiated with card networks” is another potential myth you might hear. Unfortunately, they cannot. Interchange fee reduction is impossible unless you can get the card network to change your MCC code.

Visa, Mastercard, Discover, and Amex cannot negotiate individual rates with merchants. In fact, they don’t even really do business with you directly, as much as they work with you through your payment processor.

“Flat-rate pricing is always cheaper than interchange-plus.” Wow. This one is a huge whopper worthy of the Burger King menu. If flat rate pricing was the cheapest option, corporations like Target, Costco, and Walmart would use Shopify online and Stripe terminals in their stores. But you don’t see that type of hardware in-store or those payment gateways online. That’s because once businesses hit a “normal” sales volume, interchange plus pricing is the way.

Conclusion

This concludes our brief tour of “assessment, markup, and interchange fees explained.” Unlike the monolithic nature of flat rate or bundled pricing, pass-through pricing passes the actual fees on to you with full transparency.

There is more room to negotiate better markup from your payment processor. You will also find that your fees are significantly lower than those of all your credit and debit card transactions. If you’re not yet experiencing the savings of pass-through pricing, let’s talk.

Frequently Asked Questions About Pass-through Fees

Pass-through fees are transaction fees directly passed on to the business owner from various parties involved in a card transaction. They represent a transparent and often cost-effective way for businesses to handle credit card processing costs.

Flat-rate pricing applies the same fee to every transaction regardless of the card type, which can lead to higher costs. In contrast, pass-through pricing is more transparent, it varies based on the card used, transaction type, and other factors, resulting in more cost savings.

Pass-through fees include:

– Interchange Fees: Charged by the card issuer based on card type and transaction characteristics.

– Assessment Fees: Charged by card networks like Visa and Mastercard to cover their operating expenses.

– Processor Markups: Charged by the payment processor for their services, including fraud protection and customer support.

Your businesses can minimize pass-through fees by:

– Negotiating better markup rates with your processor.

– Encouraging debit card transactions over credit card transactions.

– Using Level 2 and 3 data protocols for B2B transactions.

– Applying surcharges for certain high-fee credit cards, where allowed.

For businesses with high transaction volumes, pass-through fees are typically advantageous. However, low-volume businesses may find more benefit to flat-rate pricing.

Businesses with higher transaction volumes or those who frequently process B2B payments generally benefit most from pass-through pricing.